Rapattoni’s MLS services are being restored following cyber attack

Rapattoni, the multiple listings service software provider that was crippled in a cyber attack earlier this month, is back online in multiple markets. Service is expected to be restored to all of Rapattoni’s clients by the end of the day, sources told HousingWire. The outage, which has disrupted agents’ workflow since the attack on Aug. 9, impacted an estimated 5% of agents across the country. The cyber attack left real estate agents unable to add or remove listings, update statuses or access key information about other members. Emails and phone calls to Rapattoni, which powered MLSs in 12 markets, were not returned Wednesday.The MLS of the San Francisco Association of Realtors has been up and running since 9 a.m. this morning, said Walt Baczkowski, CEO of SFAR.The Lynchburg Association of Realtors told members that core services were restored on Tuesday, though not all features had been back online. Service was also restored for real estate agents in Indiana and Cincinnati as well, sources said.Rapattoni’s services provide agents with a single sign-on portal, granting access to tools such as ShowingTime, Cloud CMA and iMapp. During the outage, agents, MLSs and brokerages came up with solutions to weather the storm. Last Friday, eXp Realty rolled out a solution in collaboration with Northstar, one of the nation’s largest MLSs, to get its listings online. The company was able to help its 4,000 agents that were impacted by the attack. The Multiple Listing Service of Greater Cincinnati (Cincymls), for example, already announced in a Facebook post that it had selected another vendor, Perchwell, for its MLS services, and would be using Rapattoni for reading purposes only. However, Cincymls had started to look into Perchwell long before the cyberattack, association leaders said. The MLS of the San Francisco Association of Realtors started working with Zenlist, which is helping them put together a mobile app. Other sources said that they were looking into Corelogic‘s Matrix MLS.

Read MoreNew home sales grow, even with higher mortgage rates

Builders are taking advantage of the housing market inventory issues, which is why new home sales are growing yearly, even with higher mortgage rates. Today, the U.S. Census and Department of Housing and Urban Development reported that new home sales grew faster than anticipated as the builders who are efficient are finding ways to sell homes in this higher mortgage rate environment. I often use the term efficient home sellers to describe the home builders in this low inventory environment. What do I mean by efficient home sellers? Builders sell their homes as a commodity, unlike existing homeowners. Because of that, builders now have excess profit margins to use post-COVID-19, and they use it to make deals to move homes. Not all the homes being sold have price cuts or rate buy-downs. However, when the builders need to move product, they will not hesitate to make these deals happen, whereas an existing homeowner might not.New home salesAccording to the recent Census report, “Sales of new single‐family houses in July 2023 were at a seasonally adjusted annual rate of 714,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 4.4% (±12.8%) above the revised June rate of 684,000 and 31.5% (±16.3%) above the July 2022 estimate of 543,000.”As we can see in the chart below, new home sales are growing, even with the negative revisions we have seen in the report. While existing home sales are still negative year over year, new home sales are growing year over year. While new home sales market is small compared to the existing home sales market; their buyers are older and make more money.New Home SupplyNew home supply is a more complicated matter. There needs to be more clarity on how many active listings this sector can supply in the U.S. Currently, we have 75,000 new homes ready for sale. We are almost back to pre-Covid-19 levels. One thing to remember with the chart below is that even in the worst period of the biggest housing supply crash in history, the new home completed supply stayed below 200,000. This isn’t the area to look for significant new inventory for sale, folks — it never has been. Most of the active units of supply in scale will have to come from the existing home sales market.According to the new home sales report, “The seasonally‐adjusted estimate of new houses for sale at the end of July was 437,000. This represents a supply of 7.3 months at the current sales rate.”Here’s my model for understanding the builders:When supply is 4.3 months and below, this is an excellent market for builders.When supply is 4.4-6.4 months, this is just an OK market for builders. They will build as long as new home sales are growing.When supply is over 6.5 months, the builders will pause construction. As we can see in the chart below, we have made significant progress in bringing the supply down for the builders, which is suitable for housing permits in the future. However, we aren’t below 6.5 monthly on the three-month average yet.Another topic that needs more clarification is analyzing the monthly supply data. Breaking down this data (7.3 months) into different categories is vital:1.3 months of the supply are homes completed and ready for sale — about 75,000 homes.4.3 months of the supply are homes that are still under construction — about 254,000 homes1.8 months of the supply are homes that haven’t been started yet — about 108,000 homesThe homes that haven’t been started yet are at an all-time high, and the builder’s confidence has fallen a bit lately, so don’t look for a rush to build until they have a better idea of whether they can sell these homes once they’re complete.As we can see with today’s new home sales report, it’s a different world for the builders than for existing homeowners who want to sell and move to another home. The affordability hit for homeowners is real, so the total cost to move has taken a bit out of demand because prices and rates rose so much together. This is the biggest reason new listings data has been trending at the lowest levels ever. However, the builders, for now, have been able to manage these higher rates more efficiently.

Read MoreFederal Reserve fines Regions Bank $2.95 million for ‘unsafe’ flood insurance program

The Federal Reserve System this week fined Birmingham, Ala.-based Regions Bank $2.95 million for “unsafe and unsound practices in its flood insurance compliance program and for flood insurance regulatory violations,” according to the Fed.The Board fined Regions “for its failure to effectively monitor a portfolio of home equity loans for compliance with flood insurance regulations due to changes in loan servicing platforms and third-party service providers,” noting that the bank had a pattern of individual violations of flood insurance regulations.Violations of the Flood Act require civil penalties of up to $2,000 per violation, according to the order released by the Federal Reserve Board of Governors.Over a period of more than one year, Regions “did not effectively monitor a significant number of home equity loans and home equity lines of credit subject to the Flood Act for compliance with Regulation H,” the Fed said in its action.Regulation H permits a state member bank to “make public welfare investments for the purpose of investing in, developing, rehabilitating, managing, selling, or renting residential property, provided that a majority of the units will be occupied by [low and middle income] persons,” according to the Fed.A bank spokesperson told HousingWire the issue was self-identified by Regions several years ago. “We took corrective action and remediated the issue by 2017. There was no customer impact as the matter was confined to our own internal monitoring of flood insurance policies on certain properties,” the spokesperson said. “Today, years after correcting the issue, we are pleased to now fully resolve this legacy matter.”

Read MoreTom Ferry coach on real estate recruiting in today’s market

There’s no denying that this market will last for longer than a year. It’s time to take control of your business and plan for your future. We caught up with Emily Kettenburg, a seasoned coach with Tom Ferry, at the Tom Ferry Success Summit in Dallas where she shared her insights on the current trends and challenges in the real estate brokerage world.One of the most pressing issues is the shrinking property market. “This year, 20% fewer properties will trade,” Emily notes. This means that the competition is fiercer than ever. To counteract this, brokers need to focus on two main strategies: increasing per-person productivity (PPP) and recruiting more agents. Both good business practices in any market.However, the challenge lies in finding agents who can and will produce. “Unfortunately, we’ve got that 80-20 rule. So many agents are out of business in the first five years,” Emily laments.The solution? A robust onboarding process. “Their 30-day, 60-day, 90-day new agent training super important,” she says. This is especially crucial for agents who entered the industry during the Covid era, as they might not have had the same rigorous training as their predecessors.Building a recruiting roadmapBut recruiting isn’t just about onboarding. It’s about understanding the needs and desires of potential recruits. Emily suggests a “recruiting roadmap,” that starts with understanding the company’s mission, vision, and core values. “What are you hiring to?” she asks. This roadmap also involves a gap analysis, identifying lead sources for recruiting, and refining the interview process.Data and the recruiting processEmily also touches on the importance of data in the recruitment process. “Create that avatar of who your perfect agents are… and then lean into that,” she advises. By understanding the specific attributes and needs of potential recruits, brokers can tailor their approach to be more effective. Emily recommends creating five different personas or avatars based on production numbers, years in the business, personality traits, geographic area and even community involvement. “When I first started recruiting, I looked at the agents that I had and what markets they served. Then, I asked, what market would we like to serve or grow market share?,” she says. But, in some cases, she notes, “in my small town in New Jersey, it was someone who volunteered for an organization that we didn’t have anyone that volunteered with. As an example, in Trenton hire, I had no agents who volunteered at Homefront. Homefront was an organization near and dear to my heart,” she said. So, she found an agent who was very active volunteering for the organization. And that agent brought with him an entire database of others who volunteer.”Relationships are at the heartWhile data is important, nothing replaces the human touch remains crucial. “Real estate’s a relationship business built on trust,” Emily reminds us. This means that brokers need to be proactive in building and maintaining relationships with potential recruits. Whether it’s grabbing a coffee or hosting seminars, the key is to provide value and build trust. And, she notes that brokers must know who they are recruiting. She remembers a time when she was getting a weekly call from a broker who wanted to recruit her, but when she met that broker in person, he didn’t know who she was. “The broker didn’t do his homework, which should, as the very least, mean you’ve looked at a picture of the agent,” she says.On the topic of technology, Emily believes that artificial intelligence (AI) is a tool that brokers should be embracing. “If they’re not embracing AI, they’re missing the boat,” she states. AI can help brokers refine their marketing strategies, improve their communication with agents, and even aid in the recruitment process.The world of real estate brokerage is undergoing significant changes. However, with the right strategies and tools, brokers can navigate these challenges and come out on top. As Emily aptly puts it, “We need to make sure that we’re building a culture where people want to come, and that people want to stay, and we want them to be successful.”

Read MoreSupreme Court won’t allow Republican AGs to join CFPB constitutionality suit

A coalition of 27 Republican state attorneys general led by Patrick Morrisey of West Virginia was denied the option to join oral arguments against the Consumer Financial Protection Bureau (CFPB) by the U.S. Supreme Court in a case that will decide the constitutionality of its funding source, and which could decide the fate of the Bureau itself.According to an unsigned order on Monday (as reported by Bloomberg Law), the high court declined a motion that would have allowed for the attorneys general to challenge the Bureau’s funding mechanism on grounds that it violates the Constitution’s separation of powers in the Consumer Financial Protection Bureau v. Community Financial Services Association case.In their petition, the AG coalition argued that it would make a case surrounding a “special understanding of how an unbounded CFPB can damage the consumer-financial markets—and impair the States’ own abilities to regulate those markets,” according to the reporting.The high court was unmoved, issuing its unsigned order on Monday. The ask by the AGs was unlikely to be granted, since the Supreme Court rarely admits such petitions.Joining West Virginia in the effort included the attorneys general for Alabama, Alaska, Arkansas, Florida, Georgia, Idaho, Indiana, Iowa, Kansas, Kentucky, Louisiana, Mississippi, Missouri, Montana, Nebraska, New Hampshire, North Dakota, Ohio, Oklahoma, South Carolina, South Dakota, Tennessee, Texas, Utah, Virginia and Wyoming.Oral arguments in the case are currently scheduled to take place on Oct. 3, though a final decision is not expected until sometime in 2024. Recently, certain CFPB enforcement actions have been held up pending the constitutionality decision.

Read MoreRep. Waters wants concessions in ICE-Black Knight settlement agreement

Rep. Maxine Waters, the ranking member of the House Committee on Financial Services, is concerned about the Federal Trade Commission settlement agreement that will allow Intercontinental Exchange Inc. (ICE) and Black Knight to merge.“In addition to potentially creating a housing finance conglomerate that would dwarf all other players in the industry, I remain concerned that this merger has the potential to harm consumers by displacing competing products and businesses that help mitigate rising loan origination and servicing costs, thereby pushing the dream of homeownership further out of reach for families across the country,” Waters wrote in a letter to FTC Commissioner Lina Kahn.The FTC sued ICE to block the merger with Black Knight in March saying it would stifle innovation and reduce lenders’ choices, ultimately raising costs for lenders and homebuyers.Following Black Knight’s agreement to divest and sell its Empower loan origination system (LOS) and Optimal Blue product pricing engine (PPE) to Canadian company Constellation Software Inc. to mitigate antitrust concerns, the FTC, ICE and Black Knight jointly stipulated to dismiss a federal court case, clearing a major regulatory hurdle that should allow the deal to go through.With the parties planning to come to mutually acceptable terms by August 25, Waters asked the FTC to consider three areas of protection safeguards – community benefits, antitrust protections and financial stability – as the agency negotiates any agreement with ICE and Black Knight. The housing market already faces serious consolidation and affordability concerns, the FTC should ensure the deal would avoid additional pricing pressures, Waters argued. “There is no doubt that the combined technology services business of ICE and Black Knight’s, even with planned divestitures, will affect the pricing of mortgage loans and mortgage servicing rights in profound ways.”The FTC should make it mandatory for ICE and Black Knight to establish an advisory board to review how the company is meeting its obligations pursuant to the Agreement Containing Consent Order (ACCO) – including steps the company can take to benefit the public, especially underserved borrowers and borrowers of color, Waters said.The agency should “require the ICE-Black Knight conglomerate to engage in technical assistance, partnerships, and other activities to support smaller industry players, especially diverse and mission-driven community lenders like community development financial institutions (CDFIs) and minority depository institutions (MDIs) who are effective in reaching and serving borrowers of color and other underserved borrowers.”Waters also noted ICE and Black Knight should be prohibited from “shackling” Constellation with non-compete clauses and other contractual provisions that would limit them from integrating or merging with other third parties in the mortgage technology market.Divestitures of Empower and Optimal Blue should lead to greater competition in the market, not outsized competitive advantages for the newly merged ICE-Black Knight, Waters said. “The FTC must account for how products are bundled and sold in the market and ensure that Black Knight’s sale of Empower and Optimal Blue includes all products that are necessary to keep Constellation Software Inc. fully independent and competitive.”Waters also called on the FTC to conduct a short and long-term review to assess its effects and determine whether the acquisition resulted in harm to consumers, unfair or deceptive acts.“The ACCO and divestiture should be monitored over a long period of time (i.e. 10 years) to ensure the behavior of the merging parties is consistent with the terms of the deal and a competitive marketplace and allow the deal to be reopened if any terms of the deal are violated,” the letter read.Analysts at Keefe, Bruyette & Woods expect the FTC to settle on the merger deal with ICE and Black Knight.ICE and Black Knight’s agreement to sell its Optimal Blue business leaves the FTC with a weak case as it remedies the remaining horizontal overlap cited in the FTC’s complaint with a competitive buyer, Ryan Tomasello, managing director of KBW, said in the note published in July. The agency also lost several other high-profile antitrust cases in recent months.

Read MoreVlad Stojanovic joins Christie’s International Real Estate

Vlad Stojanovic, formerly of Compass, is joining the Beverly Hills office of Christie’s International Real Estate, the company announced Wednesday. The 15-year industry veteran is known for his connections to the tech and private equity sectors and boasts a track record of noteworthy transactions. Over the past two years, properties he’s sold ranged in price from $1 million to $35 million, according to Realtor.com.Among his transactions, Stojanovic successfully closed high-end condominiums, luxurious apartment buildings and luxury homes. Stojanovic’s transactions included: 29060 Cliffside Drive, which sold for $35 million; 1148 Napoli Drive, which fetched $20 million; 535 Ocean Ave, which commanded $15.7 million; and 225 North Bristol Avenue, which sold for $12.8 million. The realtor ranked 23rd in the 2023 RealTrends ranking with $64,770,044 in sales volume, making him one of the the top agents in Los Angeles. He amassed $600 million over the course of his career.“I am thrilled to be joining Christie’s International Real Estate, an organization that epitomizes excellence and has consistently delivered exceptional results in the luxury real estate market,” Stojanovic said in a statement. Aaron Kirman, founder and CEO of Christie’s, highlighted Stojanovic’s talent for “expediting property transformations.” Owing to his family office connections, Stojanovic “unlocks the doors to the world’s most exclusive properties,” the company said.

Read MoreNew home sales picked up significantly in July. Can it last?

After a slump in June, the sales pace of new homes picked up month over month in July, according to data published on Wednesday by the U.S. Census Bureau and the Department of Housing and Urban Development (HUD). In July, the sales pace of new homes climbed 4.4% compared to June, reaching a seasonally adjusted annual rate of 714,000. On a year-over-year basis, new home sales were up 31.5%.This aligns with mortgage application data for new builds, which showed demand up 35.5% year-over-year in July and up 0.2% from June.Building activity continues to be buoyed by a strong and steady demand, but there could be a shift underway in the housing market, warns Bright MLS Chief Economist Lisa Sturtevant. Two factors are at play here: high mortgage rates, which, currently around 7.5% are likely to price out many prospective homebuyers this fall, and inventory, which is beginning to tick up in many markets. However, the rate of supply for new homes still surpasses that of existing homes. “Although there is just 3.3 months of supply of existing homes, that level has been increasing for the past few months. For new homes, there is 7.3 months of supply,” detailed Sturtevant.The seasonally‐adjusted estimate of new houses for sale at the end of July was 437,000. At the current sales pace this inventory represents 7.3 months of supply, which is a decline from the 7.4 months of supply recorded in June and 2.8 months below July 2022.Regional breakdownIn the Midwest and West regions, transactions saw double-digit monthly gains. The pace of sales jumped 31.5% above the same month in 2022. In fact, all regions of the country posted double-digit improvements from a year ago. Southern metros saw a majority of newly built homes this year, as many people migrated towards the region, noted George Ratiu, chief economist at Keeping Current Matters. At the same time, the Northeast region also experienced a noticeable pickup in activity. Mid-sized markets that offer proximity to major employment centers and relative affordability saw strong demand.Homebuilders are making new homes more affordableAs the sales pace picked up month over month, the median sales price of new homes also ticked up in July, climbing $21,300 to $436,700. It was up 4.8% from June, but down 8.7% from last July. Still, it was the largest monthly increase since September 2022. The average sales price was $513,000. New home prices have been declining year-over-year for the past four months, smoothing the affordability crisis, noted Sturtevant. In fact, in July 2023, 40% of new houses were sold for less than $400,000. A year earlier, 33% cost less than $400,000, remarked Holden Lewis, home expert at NerdWallet.“Some home builders have edged prices down slightly, but builders also are increasingly offering concessions, builder financing, or upgrades to help entice buyers,” Sturtevant added. While prices are marginally declining, economists also noticed that smaller homes were coming to market this year in response to shrinking affordability. According to Ratiu, that trend should continue for the balance of the year.Can this strong builders’ activity last ? In August, the homebuilder confidence index declined for the first time in 2023, signaling headwinds looming in the sector. “In the near term, a lull in demand brought on by 7% mortgage rates could mean that builders will see less traffic and more empty model homes in the latter half of 2023,” said Sturtevant.Doug Duncan, chief economist at Fannie Mae, said the new home sales report was in line with expectations. But mortgage rates are the X factor. “Given that mortgage rates have again risen above 7 percent, we believe the risk to new home sales is to the downside. Of course, this may be partially offset as a rise in completed inventories may lead builders to offer more generous concessions to bolster demand.”

Read MoreBetter closes merger with SPAC Aurora, unlocks $565M in fresh capital

New York-based digital lender Better.com announced Wednesday the closing of its business combination with the special purpose acquisition company (SPAC) Aurora Acquisition Corp,, ending a two-year journey to make the business public. Better HoldCo, Inc. and Aurora are creating Better Home & Finance Holding Company, which will have Class A common stock listed on the Nasdaq under the ticker “BETR” starting Thursday. The deal will unlock $565 million of fresh capital for an unprofitable company. (Better.com incurred an $89.9 million loss in the first quarter of 2023, per Securities and Exchange Commission (SEC) filings.)The capital infusion includes a $528 million convertible note from affiliates of SoftBank and additional common equity from funds affiliated with NaMa Capital (formerly Novator Capital). Vishal Garg, Better.com’s CEO and founder, said in a statement that Better.com’s “journey is far from complete,” and the company will “continue pushing the boundaries of innovation in homeownership for our customers and shareholders.” Garg will be a director at Better Home & Finance, the same position as Prabhu Narasimhan and Arnaud Massenet, managing partners of NaMa Capital. Meanwhile, Harit Talwar will be the chairman of the board of directors at Better Home & Finance. “Over the past two years, Aurora has worked to deliver over $1.3 billion to Better’s balance sheet,” Massenet said in a statement. Since the deal announcement, Better’s employment count dropped from 11,000 employees in 2020 to 950 workers as of June 2023. Better faced the deterioration of the mortgage market due to surging rates. It also dealt with the bad press after Garg laid off employees via Zoom in December 2020. In an interview with HousingWire, Garg said the company has shifted its strategy ahead of its IPO. Better plans to be a mortgage marketplace that sells its technology platform to other companies. “Our overall model has changed from being a one-stop-shop, where we do everything in-house, to being a one-stop-shop where we do the things in-house that we’re the best at,” Garg said. “For things like homeowner’s insurance, title insurance, and realtors, we’ve now just become a marketplace. We match the consumer to the product with a partner capable of delivering the best product to them.”Better partnered with Palantir to create the proprietary loan platform Tinman Marketplace in August 2022.In January 2023, Better announced a One-Day Mortgage. The product allows customers to go online, get pre-approved, lock their rate and get a binding mortgage commitment letter from Better Mortgage within 24 hours.Better claims that it funded more than $100 billion in mortgage volume in six years since launch.

Read MoreDespite Some Slowdown, The San Diego Housing Market Is Looking Stable In 2023

Find out how the San Diego housing market is doing in 2023 and if there are any signs of a potential crash.

Read MoreFirst-time homeownership surges: Half of all home buyers are making their first purchase

Foreclosure inventory hits 15-month low in July

Foreclosure inventory hit a 15-month low in July representing the continued strength of mortgage performance.Loans in active foreclosure fell to 220,000 – the fewest since just after the end of federal foreclosure moratoria – and were down 63,000 or 22% from February 2020, prior to the pandemic, according to Black Knight’s mortgage performance statistics.July’s foreclosure starts of 26,300 were 4% below the average number of such actions over the preceding 12 months and remain 39% below pre-pandemic levels.Foreclosure starts equated to 5.6% of 90+ day delinquencies – still more than three percentage points below pre-pandemic foreclosure referral rates. July’s foreclosure sales (completions) of 6,100 nationally were down 11% from June. “Both serious delinquencies falling to their lowest levels since the pre-Great Financial Crisis era along with foreclosure inventories falling to a 15-month low speak to the continued strength of mortgage performance and the long-term financial benefits received by borrowers that were able to lock in record low 30-year rates for the life of their loans in recent years,” Andy Walden, vice president of enterprise research and strategy for Black Knight, said. Prepayment activity fell under easing seasonal home buying pressure along with interest rates briefly rising above 7% and ending July at 6.88%. Prepayment was still down 28% from July 2022. National delinquency rate edged up 9 basis points in July to 3.21%. But compared to the same period last year, it was down 12 bps.Serious delinquencies – which refer to 90+ days past due – continued to improve, falling to 468,000 – the lowest level seen since the pre-Great Financial Crisis housing market peak and down 161,000 (-26%) from July 2022. Mortgages that were delinquent by 30 days rose by 35,000 in July, with 60-day delinquency climbing by 17,000 (6.4%).“With early-stage delinquencies among more recent originations trending higher and economic uncertainty on the horizon, mortgage performance will be worth tracking closely as we move toward the tail end of 2023,” Walden noted.

Read MoreBHGRE President Ginger Wilcox to take the stage at HW Annual 2023

Ginger Wilcox’s intricate knowledge of the housing market is almost unparalleled. Her industry experience is vast and includes leadership roles across the housing landscape. Wilcox has a unique skillet and is laser-focused on how to best serve the end consumer. A look at her list of accomplishments includes serving as the head of industry marketing and relations for Trulia, co-CEO and chief revenue officer at RealSure and chief experience officer at Homepoint.Now, she has recently been appointed president of Better Homes and Gardens Real Estate (BHGRE), where she is tasked with leading the company’s global network of more than 12,000 affiliated brokers and independent sales associates. This extensive background in housing is simply one reason why she’s joining the powerful line-up of HW Annual speakers. As for the other reasons, the Q&A below gives a deeper look at her goals as a leader, and how much you can learn from her leadership mindset by joining us in Austin, Texas. Click the button below to register for HW Annual and keep reading for the inside conversation with Wilcox. RegisterHousingWire: Today’s uncertain market offers many growth opportunities. What is the BHGRE growth plan to boost market share?Ginger Wilcox: We’re in a unique position to really leverage what I would call the cachet and awareness of a 100-year-old brand that really is synonymous with home and has been for over 100 years. This is absolutely an advantage in today’s market and the low inventory landscape. There are fewer transactions because our agents have that kind of insight track of consumer needs and preferences when it comes to home. The way I like to think about this is if we’re on a seller shortlist to represent their home, there’s no reason we shouldn’t be winning that listing simply because of the tools, resources and insights that we have. We’re really fortunate to have a relationship with Better Homes and Gardens magazine, which gives us enormous reach, but it also gives us really unique insights into what consumer behavior looks like and the trends that are related to home. Last month, we took advantage of our 15th anniversary to showcase the value of the brand to the industry which was extremely well received. One of the things that we did as part of that was launch a “dream patio set” sweepstakes that has generated 12,000 entries. So, people are really excited about the brand and we’re going to continue to leverage that.HW: In an age where brand awareness is everything, what are you doing to make BHGRE stand out among the competition? How are you bringing new life to the brand?GW: The way that I like to think about Better Homes and Gardens is that it’s an iconic brand but it’s also the brand for the next generation. I think that’s really key because part of what I’ll be doing is leveraging my unique background to be able to bring a different lens when it comes to the digital landscape technology and how that incorporates different types of tools and resources that our competition isn’t using.HW: Your previous roles have focused on marketing and digital engagement, how has that foundation helped you take charge as President of BHGRE?GW: I have a pretty deep marketing and digital background. I’ve been the chief marketing officer and chief experience officer for companies in the mortgage and real estate space. What that means is that I spent a lot of time thinking about the evolution from print to digital. I was an early employee at Trulia, and that was a really incredible opportunity to see the industry’s transformation as we went through it. I was also co-founder of an organization that provided social media, education and training to the real estate industry. And through that, I was an early adopter of the social and digital tools and had the opportunity to partner with the National Association of Realtors to rewrite their e-PRO certification course. Through that opportunity, I gave agents new resources and tools on using digital media, social media and video technology, and all of these are tools that become really important in today’s landscape and something that we really look to lean on. With Better Homes and Gardens, we have a very strong social media presence and digital footprint and that’s an area where I really am looking forward to leaning in and diving into better support for our agents.HW: How has the experience been of stepping into your predecessor — Sherry Chris’s — shoes?GW: I’ve been pretty vocal about saying that, I’m not necessarily stepping into her shoes because the shoes are pretty hard to fill. I’m really looking forward to guiding the brand into its next chapter. I’m very lucky. I’ve known Sherry for over a decade and I have her full support as I move into my position.She’s by my side as I need her, and she’s been really generous with her time. We’ve traveled together, met with brokers and agents, and I will continue to lean on her as I need. She’s an incredible mentor and friend, but I’m really looking forward to forging a new chapter for Better Homes and Gardens and really helping us go to the next phase of our evolution and growth.HW: You’re speaking at the Vanguard Forum at HW Annual, why do you think it is important for the most successful leaders in housing to have the chance to all meet in the same room? What are you hoping your time on stage accomplishes?GW: I’m really excited to attend the event. I think that this event is unique in the industry because it brings together mortgage and real estate, which is something that’s core to my background. I’m excited to be a bridge for that. There’s going to be a tremendous audience of some of the strongest leaders in the industry, and I’m excited to listen and learn from them, as well. I think that we’re at a really challenging time in our market and a challenging time in our industry. And together we have a big opportunity to work together to move the industry forward and in some meaningful ways. HousingWire Annual Get ready for HousingWire Annual 2023 Improving your bottom line at HW Annual Marketing leader Jon Lyons to speak at HW Annual HW Annual is HousingWire’s capstone mortgage event, connecting leading professionals from the housing economy seeking to grow, innovate and win market share. This is where strategies are formed, deals are inked and lifelong relationships are solidified. Remember, HW+ members receive special perks like 50% off your admission to HW Annual, so go here to become a member. Haven’t received a discount code yet? Reach out to us at events@hwmedia.com. Join us in Austin, Texas October 10-12 for community, content and commerce.

Read MoreNo.1 agent in Georgia moves to Ansley Christie’s

Atlanta-based Christie’s International Real Estate franchise affiliate Ansley Christie’s International Real Estate poached Georgia’s top performing agent Shirley Gary and 25 of her agents, the company announced in a press release on Thursday.Gary and her agents are coming from an Engel & Völkers franchise she previously owned which had offices in Buckhead and north Fulton County, Georgia. Agents moving to Ansley Christie’s served clients in Buckhead, Midtown, Sandy Springs, Roswell, Milton, Marietta, Alpharetta and the mountain resort town of Blue Ridge, about 90 miles north of Atlanta. The combined volume of the former Engel & Völkers agents who joined Christie’s this week is more than $333 million.“We’re thrilled with the possibilities to grow our business and provide additional value to our clients,” Gary said in a statement.For the last nine years, Gary has been Engel & Völkers’ number one agent in the Americas, based on the number of closed transactions.In 2022, she closed 263 transaction sides and was responsible for $191.421 million in sales volume, milestones that pushed her to the No.1 spot in Georgia in the 2023 RealTrends America’s Best Rankings.“I’ve always been impressed with the way Shirley built and ran her business, and I knew that if she had access to the resources and support that we’ve gained over the past couple of years through our partnership with Christie’s International Real Estate, the impact for her would be exponential,” Bonneau Ansley, the founder and chairman of Ansley Christie’s, said in a statement.

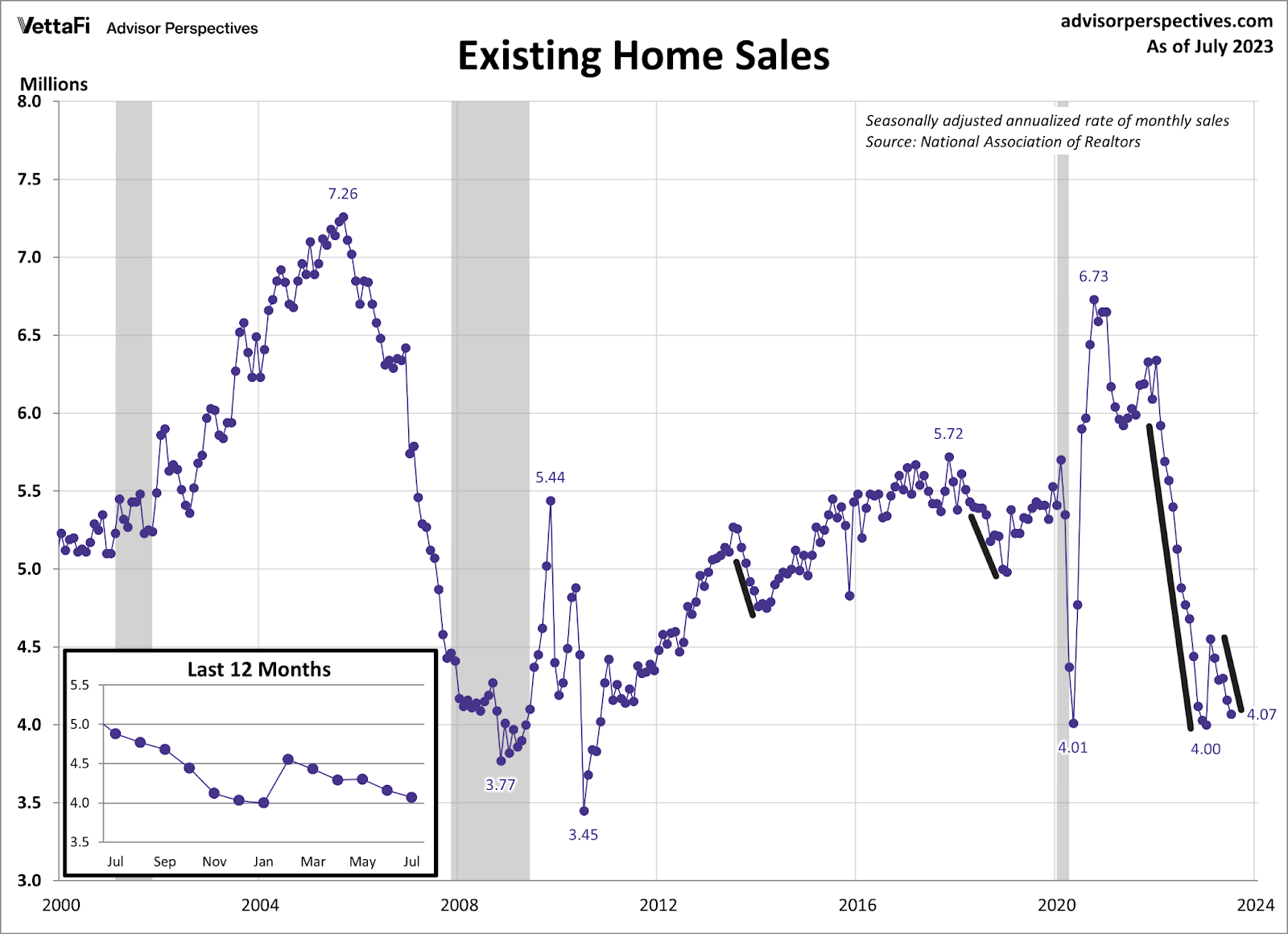

Read MoreExisting homes sales market falls again, market lacks sellers

“Home sellers are buyers” — this is a phrase that I have been using in my economic work to explain the reality of the housing market recently. Obviously, people don’t sell a home to be homeless. So, when home prices and mortgage rates rise so quickly, some sellers won’t list, which means they’re not buying either. That’s reflected in today’s existing home sales report by the National Association of Realtors (NAR), where they fell again. We are getting closer and closer to the low 4 million print we had in January.This has take us to deficient levels of demand while prices are still rising. Yes, this, my friends, is why I say the housing market is savagely unhealthy, something I discussed with CNBC last Friday. It also shows how the housing market is different this cycle than during any other housing cycle — in many decades. This is where we are heading, but unlike last year when home sales crashed, we are stuck here with low demand. Existing home sales dataAccording to the NAR, total existing-home sales — completed transactions that include single-family homes, townhomes, condominiums, and co-ops — waned 2.2% from June to a seasonally adjusted annual rate of 4.07 million in July. Year-over-year, sales slumped 16.6% (down from 4.88 million in July 2022). “Two factors are driving current sales activity – inventory availability and mortgage rates,” said NAR Chief Economist Lawrence Yun. “Unfortunately, both have been unfavorable to buyers.”As we can see in the chart below, since 2010, whenever rates rise, demand falls. When rates fall, demand picks up again. What happened with existing home sales in February was that we had three months of positive purchase application data as mortgage rates fell from 7.37% to 5.99%. We had a massive one-month print from 4 million to 4.5 million. After that, little has been happening with existing home sales — mortgage rates and home prices are too high to push growth. No movement in purchase appsPurchase application data year to date has 16 negative prints versus 14 positive prints and one flat print. So, there is little movement in either direction. If I swing back to November 9, 2022, then we have 21 positive prints. Hopefully, this shows you the power of forward-looking purchase apps data, which aren’t collapsing currently, but they’re not growing either. We are stuck at deficient levels but heading lower as mortgage rates have risen. Now let’s look at the buyer profile and the days on the market. Days on the market are growing year over year, positive for housing, but still too low for my taste. You must understand that days on the market are seasonal, so we will be entering the timeline when the days on the market will grow. The key is to focus on the year-over-year data rather than the seasonal fall and rise.@NAR_ResearchFirst-time buyers were responsible for 30% of sales in July; Individual investors purchased 16% of homes; All-cash sales accounted for 26% of transactions; Distressed sales represented 1% of sales; Properties typically remained on the market for 20 days. #NAREHS“Total housing inventory registered at the end of July was 1.11 million units, up 3.7% from June but down 14.6% from one year ago (1.3 million). Unsold inventory sits at a 3.3-month supply at the current sales pace, up from 3.1 months in June and 3.2 months in July 2022,” according to NAR.Historical inventory levelsEven with the biggest one-year sales crash ever, NAR-reported inventory levels are still near all-time lows. If most home sellers are buyers, then when they list their homes, they know they’re qualified to buy a home at current rates. Hopefully, this explains why we still have low active listings data. Traditionally, we have between 2-2.5 million active listings, currently at 1.11 million. NAR Inventory data going back to 1982.Today’s existing home sales data shows that we were slowing down again — even before the recent move in higher mortgage rates. However, home sales aren’t crashing like in 2022, and inventory has been negative year over year for some time now. This is a much different housing cycle than the ones we have seen in previous decades. The 30-year mortgage and low total housing cost has made the American home not only the best hedge against inflation but a hedge against an aggressive Federal Reserve. Remember, sellers are buyers, and we lack both to push more housing demand in the existing home sales market.

Read MoreTrade groups warn of “unintended consequences” from proposed AVM rules

The Mortgage Bankers Association (MBA) and the Consumer Bankers Association (CBA) sent a letter to regulators on Monday warning of the “unintended consequences” of new quality control standards for automated valuation models (AVMs). On June 1, six federal agencies requested comments from the public on a rule designed to ensure the credibility and integrity of models used in real estate valuations. The proposed rule will implement quality control standards that govern AVMs used by originators and secondary market issuers in valuing the real estate collateral securing mortgage loans.The agencies intend to tackle two challenges evident during the Covid-years refi boom: higher costs due to appraiser shortages and concerns regarding bias in home valuations. In their letter, MBA and CBA said that AVMs and technologies like them can alleviate appraiser shortages, reduce transaction costs, and safeguard against individual appraisal bias. Ultimately, a robust regulatory framework continues to be a critical imperative to achieve these outcomes.However, any regulation should consider the practicalities of model risk management and its potential unintended consequences. For example, the associations said the proposed rule includes Fannie Mae and Freddie Mac to the new standards, which creates a level playing field in the market. But the trade groups are worried about the impact of quality control standards on the GSEs’ alternative valuation methods, such as desktop appraisal, since these tools are essential in times of high demand. “MBA and CBA suggest that the agencies consult with the GSEs to ensure that application of the quality control standards would not create adverse effects on the availability of alternative valuation methods,” the letter states. In addition, regulators should be aware of any unbalanced market effects of AVMs regulations, conflicting interpretations of the legal framework, and the lack of established methodologies in examining systemic bias in the U.S., the trade groups state. The agencies involved include the Federal Housing Finance Agency; the Consumer Financial Protection Bureau; the National Credit Union Administration; the Federal Deposit Insurance Corporation; the U.S. Department of the Treasury; and the Federal Reserve System.Per the proposed rules, each institution using AVMs will adopt and maintain its practices, procedures, and control systems, reducing the burden on smaller institutions. But the trade groups request the agencies to include a small lender/servicer exemption from the standards, as these companies are likely to rely on larger outside service providers subject to a thorough review by regulators or larger clients. Regarding third-party providers, the associations suggest that the CFPB expand its Compliance Bulletin 2016-02, Service Providers to outline expectations and potential recourse “for quality control and fair lending oversight” of third-parties providing AVMs services. In addition, MBA and CBA said that creditors should not be liable for violating nondiscrimination law when relying on third-party AVMs, disagreeing with the agencies’ interpretation of the Fair Housing Act. The MBA and the CBA requested an adequate implementation timeline of at least 12 months. The White House supports a new rule for AVMs, which follows goals set out by the president in addressing issues of racial bias that have exacerbated homeownership and wealth gaps. When announcing the proposed rule, Vice President Kamala Harris weighed in.“Today, I’m proud to announce we are developing a rule that will require that financial institutions ensure that their appraisal algorithms are not biased, for example, that they do not produce lower valuations for homes owned by people of color,” Harris said. “We are also releasing the guidance to make it easier for consumers to appeal what they suspect to be unbiased valuation.”Another trade group weighed in on the newly proposed rule. The National Association of Mortgage Brokers (NAMB) said it supports new federal regulatory proposals governing the use of AVMs. “The reality is the systems and structures are themselves, in some cases, problematic,” said NAMB President Ernest Jones in a statement. “Even when appraisers follow the intended approach, it may result in an outcome that disenfranchises people. They could be doing everything in a way they feel is consistent with the approaches they’ve learned and for which they’re certified, but there are some underlying issues that need to be addressed.”

Read MoreHome sales drop in July as high interest rates spook buyers

The housing market continues to cool amid high mortgage rates, low inventory and rising property insurance rates.The National Association of Realtors (NAR) suggested a 2.2% month-over-month drop from June, a seasonally adjusted annual rate of 4.07 million, according to its latest report.Despite a sharp drop in home sales compared to the year-earlier period, the median existing-home sales price rose 1.9% from one year ago to $406,700. It was the fourth time the monthly median sales price exceeded $400,000, according to the NAR.While all regions saw sales activity decline, the Northeast region saw the biggest drop in home sales, with existing-homes sales down 5.9% month over month and 23.8% compared to July 2022. The median price for a home was $467,500, up 5.5% a year ago. By contrast, the West saw existing-home sales increase 2.7% since June, to an annual rate of 770,000 in July, down 12.5% from the prior year. Median home prices there were roughly unchanged from the same period in 2022.Elevated mortgage rates and low inventory As of August 17, mortgage rates surpassed 7% as U.S. bond yields hit their highest level since 2008. Average mortgage rates rose by about a half percentage point in May and June, pricing some buyers out and limiting closed sales in July. With supply remaining low — with less than three months of supply nationally — some buyers may continue to rent, especially in markets where rents are falling, said Lisa Sturtevant, chief economist at Bright MLS.Despite market pressures, however, Zillow Senior Economist Jeff Tucker suggested that price trends are “swinging the pendulum of negotiating power back in favor of those buyers who remain in the hunt.”Others say it will take time for home prices to drop. Realtor.com Chief Economist Danielle Hale said consumer incomes will need to catch up for the market to recover next year.“Fortunately, inflation is ebbing, and a further decline in July asking rents will likely help keep that trend on track,” he added. Homes are sitting on the market somewhat longer. Properties typically remained on the market for 20 days in July, up from 18 days in June and 14 days in July 2022, according to the NAR.

Read MoreOpinion: Title companies committed to promoting homeownership for all

Prospective homebuyers face an obstacle course of challenges – from financing to logistics – once they make the decision to purchase a home. This process can be even more difficult to navigate for those with limited financial resources, first-time homebuyers, and minority borrowers, especially in today’s competitive real estate environment in which prices are high, homes sell fast, and supply is at an all-time low.That is why it is critical that the title insurance industry — alongside our industry partners — has made it a priority to help more Americans benefit from homeownership by making the process more affordable and accessible.Fees add up in transactionWhile the cost of title insurance is less than .5% of all loan charges, the industry understands that fees can add up in a real estate purchase. Title companies are committed to doing their part in promoting affordable and sustainable housing initiatives and finding ways to address cost. ALTA member company CATIC, for example, adopted a program that offers a 10% discount on title insurance premiums for first-time homebuyers in Massachusetts. This initiative aligns with MassHousing’s new loan product, Workforce Advantage 2.0, which seeks to overcome the racial disparity in homeownership in Massachusetts.Although there are many programs available to help first-time homeowners, keeping these programs well-funded can pose a challenge. Another ALTA member, Pioneer Title provides information to its customers about the Northern Arizona Housing Fund, which awards $25,000 grants for specific housing-related opportunities. Pioneer allows donations to be made to the fund at the close of all transactions and matches all donations.Partnerships make a differencePartnerships between the industry and housing nonprofits are also making a real difference to individuals seeking affordable housing. ALTA established the ALTA Good Deeds Foundation in 2020 to help title professionals best support and give back to their local communities. In three years, ALTA has allocated more than $712,000 in grants to 121 community nonprofits in 38 states, as well as Washington, D.C. A significant number of grant recipients are affordable housing organizations that support low- and moderate-income households.Making sure the potential homebuyer is educated is an important part of increasing homeownership opportunities, especially to first-time homebuyers. ALTA has a website dedicated to informing consumers about the closing process and the benefits of title insurance. We’re also in the process of translating content into many different languages to better serve all potential homebuyers.Operational barriersWhile affordability remains the biggest hurdle to homeownership, operational barriers have also made it cumbersome to complete a real estate transaction. During the pandemic, the title industry advocated for the expansion of access to digital closings through remote online notarization (RON). Through RON, homebuyers with disabilities, those serving overseas, and those living in underserved, underbanked communities can finalize their real estate transactions fully remotely.Currently, 44 states have enacted laws allowing access to RON. At the federal level, Congress is considering the SECURE Notarization Act, a bipartisan federal bill to approve the use of RON nationwide with strong consumer protections, which ALTA continues to support.As an industry, we believe homeownership should not just be a privilege for a select few. We are committed to making homeownership both more affordable and accessible for everyone. Alongside our industry partners, we will never stop identifying new ways to make the dream of homeownership a reality for more Americans. Diane Tomb is CEO of the American Land Title Association, the national trade association representing the land title insurance and settlement services industry, which employs more than 120,000 people working in every county in the United States.

Read MoreMortgage forbearance improves in July

The total number of loans now in forbearance decreased by 5 basis points to 0.39% of servicers’ portfolio volume in July from 0.44% May, according to the Mortgage Bankers Association’s (MBA) monthly loan monitoring survey.The MBA estimates about 195,000 homeowners are in forbearance plans. Mortgage servicers have provided forbearance to about 7.9 million borrowers since March 2020.The prevalence of forbearance plans has dropped dramatically since 2020 and the reasons that borrowers are in forbearance are changing, the MBA said.“About two-thirds (69.3%) of borrowers are still in forbearance because of the effects of COVID-19, but a growing share of borrowers are in forbearance for other reasons that cause temporary hardship such as financial distress (24.2%) or natural disasters (6.5%),” Marina Walsh, MBA’s vice president of industry analysis said.”“With the COVID-19 national emergency lifted, Fannie Mae and Freddie Mac recently announced the retirement of certain COVID-19 flexibilities relating to forbearance plans and workouts. Given the recent natural disasters impacting California, Washington, and Hawaii, forbearance is one way for mortgage servicers to mitigate the potential impacts on homeowners,” Walsh added. Sorted by investor type, the share of Ginnie Mae loans in forbearance decreased 13 bps to 0.80% in July and the forbearance share for portfolio loans and private-label securities (PLS) dropped 7 bps to 0.45%. The share of Fannie Mae and Freddie Mac loans in forbearance decreased 1 basis point to 0.20% during the same period.By stage, 36.5% of total loans in forbearance are in the initial forbearance plan stage, while 53.3% are in a forbearance extension. The remaining 10.3% are forbearance re-entries, including re-entries with extensions.Washington, Colorado, Idaho, Oregon and California were the five states with the highest share of loans that were current – not delinquent or in foreclosure – as a percent of servicing portfolio. Louisiana, Mississippi, Indiana, New York, and West Virginia had the lowest share. Total loans serviced that were current as a percent of servicing portfolio volume decreased to 96.02% in July from June.

Read MoreModernized Antique Structures Dot 52 Protected Acres In New Jersey

Its many antique buildings, including a five-bedroom main house with the original section dating back to the 1700s, have been expanded and updated to modern tastes.

Read More

Categories

Recent Posts