Florida affordable housing law that dilutes local power has upset the apple cart

A new affordable housing law passed by Florida’s legislature and signed in March by Gov. Ron DeSantis is reportedly creating anxiety among local elected officials who are concerned that the new law cedes too much control over zoning and other matters to the state government.The “Live Local Act,” passed unanimously in the State Senate and by a vote of 103-6 in the House, represents a sizable investment in housing by incentivizing developers to construct affordable housing units while restricting zoning and planning restrictions in local jurisdictions approving multifamily construction projects in order to limit bureaucratic barriers to increase supply.But some of those local officials are now expressing concern that the provisions of the new law are restricting their ability to more actively participate in development decisions within their communities, according to reporting by WUSF Public Media.“I think the hesitancy comes with the fact that it’s a preemption. I think whenever we’re talking about home rule or preemption, there’s always going to be local pushback,” Florida Housing Coalition Legal Director Kody Glazer told the outlet.The new law comes with restrictions as to how much local elected officials can influence zoning and development decisions as well as density and height restrictions. Some of these concerns have been echoed in other states that have passed restrictions on zoning in other states including Massachusetts and Washington.The Tampa metro area has experienced among the highest home price increases in the country since 2019, in large part because the counties have in place restrictive zoning policies that increase the value of land. Following antidevelopment protests from residents ostensibly concerned about local infrastructure, in late 2019 Hillsborough County placed a moratorium on the rezoning of land for housing in some areas. Two years later, Pasco County, north of Tampa, also put a moratorium on rezoning to multifamily use in some areas.The new Florida law applies to any residential housing projects that sit “on commercial, industrial or mixed-use land that allocates at least 40% of units to be affordable for residents earning up to 120% of the area median income,” according to WUSF. The law went into effect on July 1, and officials in cities including St. Petersburg and Tampa were reportedly briefed on their remaining rights overseeing such projects under the new law.The process has gone more smoothly in St. Petersburg than Tampa, where officials in the former have “already heard interest from ‘ready to build’ developers in recent weeks” based on local reporting by the Tampa Bay Business Journal. In Tampa itself, however, a city council meeting on July 13 featured sometimes tense discussions between city leaders centered on compliance anxiety with the new law.“The state is going to just gonna keep taking and taking and taking – and I’m not willing to give an inch more than I’m required to,” said Tampa city council member Lynn Hurtak, according to WUSF. She later introduced a motion to implement only what was legally required by the city to comply with the new law until the next scheduled council meeting. That motion passed.During the meeting, another city official – Nicole Travis, Tampa’s economic development director – explained that while she understood the council’s frustrations, “the new housing rules make the approval process of eligible affordable housing projects a solely administrative function that can circumvent city council,” according to WUSF.

Read MoreVa.-based Coldwell Banker Premier expands to Maryland

Coldwell Banker Premier announced a merger with Coldwell Banker Professional Real Estate Services along with all of its sales associates, which further expands Coldwell Banker Premier’s office footprint into Cumberland, Maryland, and surrounding markets. This is the sixth merger by Coldwell Banker Premier since the beginning of 2022. Coldwell Banker Premier was named a 2023 RealTrends GameChanger for its 76% transaction side percentage growth over five years (2018-2022.) The company’s COO, Stephen Meadows, was honored as a 2022 RealTrends Emerging Leader, now called Rising Stars.From left: Stephen Meadows, Liz Rhodes, Seth Loar, Steve DuBruelerThe former Coldwell Banker Professional Real Estate Services office in Cumberland, Maryland will become Coldwell Banker Premier’s 18th office and largest by agent count in the company’s Mid-Atlantic footprint, which spans Virginia, West Virginia, Pennsylvania, Delaware, Maryland, North Carolina, and Washington D.C.“I am proud of our team for enabling us to continue our expansion efforts,” said Steve DuBrueler, Founder and CEO of Coldwell Banker Premier, in a statement. “In this age of uncertainty in real estate, many brokers and owners are unsure of what their future holds. At the end of the day, we are here to build better lives for our agents and staff and having a strong foundation and expansive footprint is a key component of that”.Coldwell Banker Premier Chief Operating Officer, Stephen Meadows said, in a statement, “Our company is committed to creating stability and continuing opportunities for our agents and to be a safe haven for companies and individuals looking to shift their business in this turbulent market.”

Read MoreRedfin looks to experiment with a new brokerage compensation model

Redfin was in the red yet again in the second quarter, but its losses are narrowing and it’s tweaking its unique brokerage model to court more experienced agents in pricey coastal areas. Redfin’s financialsRevenues at Redfin fell 21% year-over-year to $275.6 million, down from $606.9 million a year earlier. The brokerage and portal’s real estate services division, its principle source of revenue, dropped to $180.6 million, a 28% decline. In all, Redfin registered a $27 million net loss for the quarter, a 64.9% year-over-year decline from the $78.1 million loss in the second quarter of 2022.Redfin’s mortgage revenue was $38.4 million, down 28% year-over-year. Its attach rate was 19%, down from the 20% last quarter.In an earnings call with analysts on Thursday, Redfin founder and CEO Glenn Kelman said high mortgage rates and a frozen existing-home sales market resulted in a slowdown for Redfin’s salaried agents and it will likely continue for a few more quarters.“Sales volume is near rock bottom,” he said.The company expects to break-even on an adjusted-EBITDA basis over the next 12 months, rather than reach that goal by the end of 2023, which Kelman described as “a setback.” He did note that company expects to improve its adjusted EBITDA this year by more than $140 million.Redfin’s market share in the second quarter of 2023 declined nearly 10% on an annualized basis to 0.75%. Revenue per transaction dropped 2.88% year over year to $10,224, the company said.Kelman told analysts that agent layoffs forced the company to reassign about a third of its active customers, and the closure of ibuying arm RedfinNow eliminated 12% of its listing demand. On a positive note, Kelman said the portal’s visitor gains increased 9% annually in the second quarter of 2023. Without naming the rivals, he said Zillow and Realtor.com declined in visitors. He also spoke of an improving the user experience with artificial intelligence and the promise of its burgeoning rental platform. A more ‘traditional’ approach to brokeragePerhaps the most interesting talking point on the call was Redfin’s embrace of what could only be described as a more traditional real estate brokerage model.Redfin is eschewing junior agents and its high-fixed cost, salaried approach in targeted coastal markets. Instead, it’s looking to hire more experienced agents in high-priced areas, and Kelman said the brokerage is targeting the San Francisco and Los Angeles markets for a pilot program.“In the San Francisco Bay Area, our share is below 2%, but the share of people who bought a home and who had earlier contacted our agents for service is nearly 30%. It’s even higher for purchases above $1 million,” Kelman said, adding that “anyone launching a brokerage today with that much demand would have a massive advantage in recruiting and retaining the best agents.” Starting in 2024, Redfin plans to give agents in the L.A. and San Francisco “the lion’s share of the commission” on self-sourced sales “while keeping for ourselves the high margins on Redfin-sourced sales,” Kelman said. Redfin’s goal, he said, is “to hire and keep agents who can deliver better service and higher close rates for Redfin-sourced customers buying homes above $1 million and incremental profits from their own sales, too.” If the pilot is a success, it will be rolled out to additional coastal markets. “This is just a more traditional salesperson who wants to augment his or her income with Redfin-sourced sales and we’re switching our existing agents in those pilot markets to this pay plan,” he said.“So, usually, the trade-off at Redfin when we approach agents is you’ll get more Redfin customers, but at a lower split. So, you have to close more sales to make the same amount of income or more income. Now, we’re trying to offer agents the best of both worlds where we allow agents to close sales from their personal network at a split with Redfin.“That’s similar to what they would get at a traditional broker while retaining the high margins on Redfin-sourced sales. So, let’s say an agent has closed 10, 15 sales in California above $1 million, they could come over to Redfin and earn about the same income, but we could help them meet customers to close another 10 or 15 sales. And that would be incremental, and that would be at the Redfin margin. This is what our competitors fear we would do.”

Read MoreMortgage rates fall after softer labor data

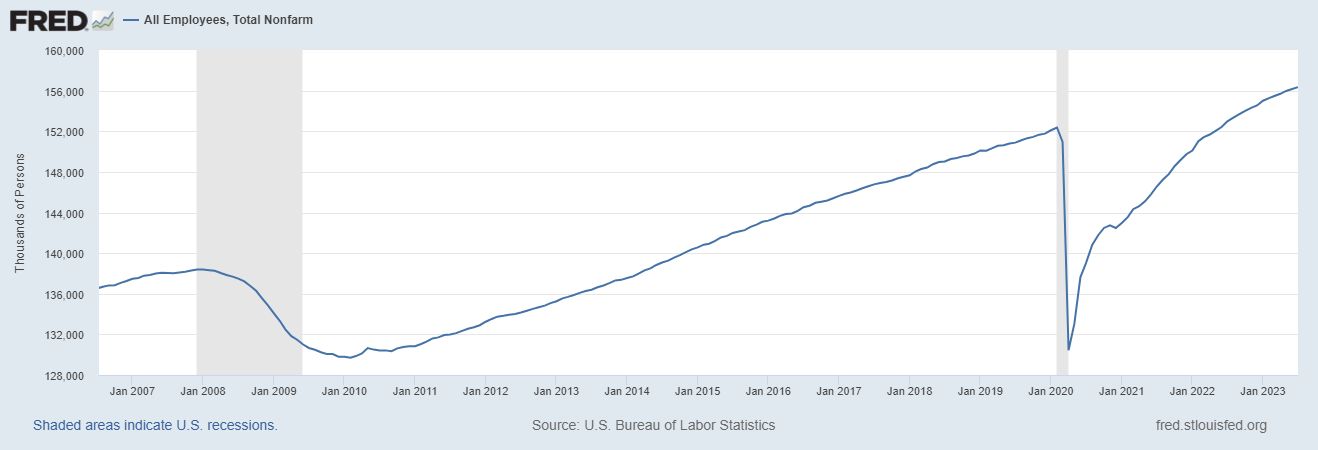

Mortgage rates are finally headed lower after a crazy week of jobs data showing that the economy isn’t going into recession. Job growth is slowing as we get closer and closer to the target range of the make-up demand in labor, but it hasn’t broken yet. What do I mean by a make-up demand in labor? Assuming we had no COVID-19 and the economy continued as it had been — which was running at the most prolonged economic and job expansion ever recorded in history — we would be between 157 million – 159 million jobs today. Currently, we are at 156,342,000, which means we are a few jobs reports away from getting into that make-up range.From BLS:Total nonfarm payroll employment rose by 187,000 in July, and the unemployment rate changed little at 3.5 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in health care, social assistance, financial activities, and wholesale trade.As you can see in the chart below, the job growth rate is slowing, as it should. We had negative revisions to this jobs report and excluding the government jobs, we are averaging 185,000 jobs added per month in the last three months. Let’s look at the report’s internals, where we gained and lost jobs, and why mortgage rates fell today.Wage growth is not spiraling out of control as some have feared; this would have been bad news for mortgage rates because that’s what happened in the 1970s. However, wage growth has stayed firm the past few months. With headline consumer price index inflation running at 3% year over year, people are seeing real wage growth again, as we have been steady at 4.4% for a few months here.The unemployment rate for those who didn’t finish high school has been pretty wild up and down lately; in this report it fell from 6.0% to 5.2%. Traditionally, those without a high school education tend to have the highest unemployment rates in any recession.In this job report, the unemployment for education levels: Less than a high school diploma: 5.2%High school graduate and no college: 3.4% Some college or associate degree: 3.1% Bachelor’s degree or higher: 2.0%The hours worked were less in this report, meaning that employers are holding onto their labor but are cutting hours. If you want to see why mortgage rates are falling today, this is one data line to keep an eye on going out for months. What other labor data did we have this jobs week?This week we had a decrease in job openings, but that number is still abnormally high for the Fed. Even though we have fallen from 12 million to under 10 million, the Federal Reserve would love to see this back toward the 7 million level. So far, no luck! Here is a look at job openings with a longer-term view, and you can see the decline from the peak.Now the quits ratio is almost back to pre-COVID-19 levels; this is a big thing for the Fed because less people are leaving work for higher wages, which they see as a positive.Jobless claims, the most important data line at this expansion stage, rose this week, but it is still far from my key 323,000 target level for the Fed to pivot.From the St. Louis Fed: Initial claims for unemployment insurance benefits increased by 6,000 in the week ended July 29, to 227,000. The four-week moving average declined to 228,250So what does this mean for mortgage rates? Today we were close to testing the high-end range for my 10-year yield 2023 forecast of 4.25%. We got as high as 4.20% but bond yields have fallen since that level. As I write this article, the 10-year yield is currently at 4.04%.The 10-year yield channel has held in my range of 3.21%-4.25%, which equates to mortgage rates of 5.75%-7.25%, assuming where the spreads were at the start of the year. This is how I traditionally forecast mortgage rates for a year, by creating a level of where the bond market should be for most of the year. If the 10-year yield closed above 4.25% today and we saw more bond market selling next week, we would need to have a new conversation about mortgage rates rising more this year than I had anticipated. However, that hasn’t happened yet.It’s been a crazy week with jobs data and the bond market. The key, for now, is that the labor market is slowing down but not breaking. We held the key line on the 10-year yield and mortgage rates went lower today, so at least for one day the housing market can say it was a good Friday. Next up is the Consumer Price Index inflation report on Aug. 10, which will be a market-mover for mortgage rates.

Read MoreTo spur affordable housing, the federal government is selling land for dirt cheap

The U.S. Department of Housing and Urban Development (HUD) and the U.S. Department of the Interior announced this week its plans to arrange the sale of federal land to the State of Nevada in an effort to spur construction of affordable housing units in the Las Vegas metropolitan area.The arrangement, codified in a memorandum of understanding (MOU) signed by both departments, establishes an arrangement to sell federal lands to the state at a rate of $100 an acre, far below the land’s market value. The sold land will be used for “the construction of critically needed affordable housing projects in Southern Nevada,” according to an announcement from HUD.“We are proud of the partnership with the Department of the Interior to help families in Nevada get access to homes they can afford,” said HUD Deputy Secretary Adrianne Todman. “This builds on the Biden-Harris Administration’s efforts announced last week to ensure an increase in housing supply to lower costs across the country.”Sen. Catherine Cortez Masto (D-Nev.) was a key player in the development of the arrangement, according to local reporting by the Las Vegas Review-Journal.“Nevada is facing an affordable housing crisis and we need to be doing more to ensure we can build more homes for working families,” Cortez Masto said in a statement. “For too long developing affordable housing on public lands in Nevada has been bogged down by an inefficient process, and I pushed for these vital improvements that will make it easier to build more homes for Nevada’s working families.”The arrangement and inter-departmental collaboration is made possible by the Southern Nevada Public Land Management Act (SNPLMA) of 1998, which “allows the Department of the Interior’s Bureau of Land Management (BLM) to sell public lands within a specific boundary around Las Vegas, Nevada, for development,” HUD detailed.Additional authority is established in a specific section of the law since the land is being sold well below fair market value.“Although SNPLMA requires parcels to be sold for fair market value to fund education, water and public lands projects in Nevada, Section 7(b) of the Act allows state and local governments to purchase land for a nominal cost to support affordable housing,” HUD said.Within Clark County – the area that contains the Las Vegas metro area – officials say that there is a shortage of approximately 85,000 housing units, echoing issues being faced across the country.“Clark County has long advocated for more land to alleviate affordable housing challenges and recently worked with the BLM to negotiate the process reflected in the MOU,” a county spokesperson told the Review-Journal. “While this took some time to be formalized, we are happy this is moving forward now to benefit our community in the long-term.”

Read MoreRE/MAX remains profitable even as US agent count drops

Despite a 10.6% annual decline in revenue and a 6.3% drop in U.S. agent count, RE/MAX Holdings, the parent company of the real estate giant RE/MAX, stayed in the black during the second quarter of 2023.Overall for the quarter, RE/MAX generated a net income of $2 million, down from $5.8 million a year ago, as its revenue dropped to $82.4 million. The firm attributed this to negative organic growth due to lower broker fee revenue and reduction in U.S. agent count, but it noted that it was partially offset by growth in Motto Mortgage and wemlo.Although the firm’s total agent count has ticked up slightly, rising 0.4% year over year in Q2 to 144,510 agents, its U.S. agent count has taken a massive hit over the past several quarters, dropping to 56,987 agents. This decrease has been somewhat offset by a 1.5% annual increase in the firm’s Canadian agent count to 25,218 agents, and a 6.9% yearly jump in its international agent count to 62,305 agents.“Canada continues to be an amazing growth story,” Nick Bailey, the president and CEO of RE/MAX, told investor and analysts during the firm’s second quarter earnings call Thursday morning. “Despite the rebalancing market, our presence continues to grow north of the border.”That Canadian agent count has grown every month of the year so far, except for January. Bailey also noted that the firm has also seen a fair share of boomerang agents in recent months, who have returned to the firm from a variety of other brokerages.RE/MAX is also pleased with its international agent count growth.“Agent count outside of the U.S. and Canada accelerated to 7% during Q2 with countries including Turkey, Peru, Brazil and South Africa adding a notable number of agents,” Bailey said. “We believe the enduring global appeal of the RE/MAX brand and the impact of our recruiting campaigns are the primary drivers of our success.”As U.S. agent count continues to decline, firm executives said RE/MAX remains focused on its growth pipelines.“The combination of higher interest rates and tight inventory has made for a challenging housing market and agent-recruiting-and-retention environment,” Steve Joyce, the CEO of RE/MAX Holdings, said. “On a positive note, the pace of our U.S. agent count losses slowed quarter over quarter — which is encouraging, given the market conditions.”Bailey also noted that RE/MAX is continuing to focus on its initiatives surrounding real estate teams.“The team pilot we launched last August is helping our affiliates gradual expand and retain existing teams and build pipelines for large teams in the five pilot states of Texas, California, Florida, Maryland and New Jersey,” Bailey said. “Whether it is RE/MAX growing to six members, large teams joining the network or existing teams staying with us at a higher rate, this initiative is showing promise.”Due to the success of the initial pilot, Bailey said RE/MAX has expanded it to Arizona, and is extending it into next year in the existing five states.Even with higher mortgage rates and fewer purchase transactions nationwide, RE/MAX Holdings reported strong quarters for both Motto Mortgage and wemlo, its third-party mortgage loan processing service.During the second quarter, Motto Mortgage reported a 17.5% annual increase in franchise sales, with office count rising to 235 offices. However, executives noted that Motto Mortgage’s annual revenue will be about $1 million less than expected in 2023 due to the uncertain mortgage rate environment.“On the mortgage side, wemlo is ramping up, and we continue to expand our Motto franchise sales operation,” Joyce said. “The addition of experienced personnel with in-depth franchise experience to our inside sales team is just one reason we are optimistic about increasing the pace of Motto franchise sales in the second half of 2023 and beyond.”Looking ahead, RE/MAX executives were optimistic about the future growth of the firm, noting that they expect agent count to remain relatively flat for the third quarter and that revenue will fall in a range of $78.5 million to $83.5 million, including marketing funds.

Read MoreLOs: Turn data assets into origination opportunities

Rates are high, housing inventory is down, and competition for new originations is fierce. Leaders across mortgage and banking are turning to their marketing partners with some variation of the same ask: “We need to improve the effectiveness and profitability of our campaigns, increase originations, and oh, by the way, budgets have been slashed — so any ideas better be cost-effective.” Easy, right?Sure, multi-million-dollar ad campaigns and exciting new lead sources would be great, but often lenders can find opportunities more efficiently by referring to the data and resources they already have. Many lenders have access to a large amount of consumer data, namely their customers and prospects, and the attributes they know about them. Here’s how to turn those existing data assets into origination opportunities, all while creating a better experience for customers. Get your data in shape. For example, Americans move on average 11.4 times in their lifetime and alerting their bank to a change of address is not always a priority, especially for those who interact with their financial institutions digitally. So, until the consumer volunteers that new address, direct mail offers are likely piling up at their old one. At scale, this can generate enormous marketing waste. If you’re relying on consumer information collected years ago, it’s good to score it for accuracy and update it regularly. Refreshing your data avoids the risk of misplaced marketing expenses and missed opportunities to engage with customers and prospects. This goes for phone, email and digital identifiers as well. To market effectively it is crucial to have accurate consumer information. Taking it a step further, consider whether data is being collected accurately to begin with, especially on lead submissions. Many consumers are, rightfully, hesitant to submit a correct phone number on a lead form. This hesitation not only hinders lenders from reaching them, but also poses a compliance risk to the business if incorrect numbers are dialed.Expand on what you know. Even if you have the right information and tools to engage customers and prospects, you likely can’t engage with all customers at all times, nor should you want to. This is where expanding what you know about the consumer comes into play. Demographic, financial, and psychographic attributes can all help in segmenting target audiences for more effective engagement and deliver a more meaningful experience for the consumer. Consider developing an “ideal customer profile” that correlates with a higher conversion rate, then find and prioritize these “ICPs” within your database. This will be significantly more effective than “one size fits all” campaigns. You can also use these insights to build out digital audiences for acquisition. It’s remarkable how many financial institutions deploy a universal model when there will be significant variation across how their prospects and customers respond to their marketing. By understanding and leveraging this variation, lenders can cut wasted spend and improve profitability. As with getting data in shape, these insights can also be leveraged at the point of lead submission to inform things like scoring, routing, and messaging from the first consumer interaction onwards. Remember that great marketing requires great timing. Most lenders leverage credit triggers to try to prevent competitive fallout, and it’s often considered table stakes for any retention strategy. However, consider this: a credit trigger means a consumer is likely applying elsewhere and solely relying on that insight is akin to showing up to the game in the fourth quarter. And because other lenders are also getting that trigger, it’s like showing up to play against five other teams. Not surprisingly, there’s even a legislative proposal to ban credit triggers entirely in the name of consumer experience. Delivering an effective and relevant consumer experience requires engaging with consumers earlier in their homebuying journey. We’ve historically seen consumers first start shopping online for a new mortgage or home around 100 days before a credit trigger, a timeline that’s expanded even further with the current rate environment and limited housing inventory. Evaluate internal and external resources that can help you determine who might be at the beginning of that shopping process. It’s going to be a long process, so create touch points to offer the consumer resources that will keep them engaged with your brand throughout their homebuying journey. Galen Foot is an enterprise account executive at Verisk Marketing Solutions.

Read MoreSEC ends investigation into Better.com and SPAC partner’s alleged securities law violations

Aurora Acquisition Corp., the special purpose acquisition company planning to make public the digital nonbank lender Better.com, said on Thursday that the Securities and Exchange Commission (SEC) ended an investigation of the companies with no enforcement action. In July 2022, HousingWire reported that the SEC launched an inquiry into Aurora and Better to evaluate allegations of federal securities law violations, prompted by a former top executive’s lawsuit. “On August 3, 2023, SEC staff informed Aurora and Better that they have concluded the investigation and that they do not intend to recommend an enforcement action against Aurora or Better,” Aurora’s SEC filing states. The lawsuit was filed by Sarah Pierce, former executive vice president for customer experience, sales and operations at Better.com. Pierce claimed the company and its CEO, Vishal Garg, violated securities and labor laws as the lender began working toward its public offering. Pierce alleges Garg told the board of directors that the firm would report a profit by the end of Q1 2022, despite Pierce and other senior leaders explicitly saying it was impossible. The lawsuit is in the discovery phase, per court filings. Aurora and Better disclosed that the SEC’s enforcement division requested documents in the second quarter of 2022 regarding Better’s business and operations and Garg’s other business activities. The company said it collaborated with the SEC. Aurora’s shareholders will decide the merger’s fate next week, on August 11, about two years after the deal was announced and ahead of the extended deadline to complete the merger deal on September 30. If Aurora is unable to complete the merger with Better by September 30, or any other business combination, it will cease all operations.Better has faced an arduous journey to its IPO, marked by surging mortgage rates and declining origination production. In the first quarter of 2023, the digital lender posted a net loss of $89.9 million, per Aurora’s filings. To navigate a challenging mortgage market, Better imposed massive layoffs, receiving bad press for the manner in which it handled the layoffs. The digital lender had about 950 team members as of June 8 — a 91% drop from its peak of approximately 10,400 employees in Q4 2021, SEC filings show. Better’s most recent business change was to shift its real estate strategy. The company will partner with outside agents as referral partners, pivoting from its in-house licensed professionals. Ultimately, Better laid off the agents in its real estate brokerage subsidiary, Better Real Estate LLC.Better ranked as the 59th largest mortgage lender in the country in the first quarter, per Inside Mortgage Finance.

Read MoreThe labor market showed signs of modest cooling in July

Data from the July jobs report released Friday fell roughly in line with expectations. Job gains came in lower than both the 278,000 monthly average for the first half of 2023 and the 399,000 average of 2022. Total nonfarm payroll employment increased by 187,000 jobs, compared to 209,000 in June, according to data released by the Bureau of Labor Statistics. The unemployment rate changed little at 3.5%, compared to 3.6% in May, with the total number of unemployed persons falling to 5.8 million. The unemployment rate has remained between 3.4% and 3.7% since March 2022.In June, job openings eased back to 9.6 million, bringing the openings rate to 5.8%. Meanwhile job quits slipped to 3.8 million or 2.4%.“The incoming economic data continue to convey conflicting signals about the strength of the economy. Indicators of manufacturing and service sector health remain lackluster, measures of inflation have moved lower, while GDP growth in the second quarter was stronger than expected and consumer spending remains resilient,” said Mortgage Bankers Association VP and Deputy Chief Economist Joel Kan.While job growth is weakening, and wage growth is holding steady, both metrics are still above the pace that would be consistent with the Federal Reserve’s inflation target, noted Kan. “However, we expect that the FOMC will hold the federal funds target at its current level given the declining trend in inflation,” he added.The lion’s share of the job growth in June came from gains in health care (+63,000), social assistance (+24,000), financial activities (+19,000), and wholesale trade (+18,000), according to the report.Employment in the construction industry continued to trend up in July, adding 19,000 jobs, especially in the residential construction space. The ongoing shortage of housing inventory helped spur an increase in home building and home improvement activity, Kan said. On average, the industry added 16,000 jobs per month in the second quarter of the year, after employment was essentially flat in the first quarter. Over the month, a job gain in real estate and rental and leasing (+12,000) partially compensated for a loss in commercial banking (-3,000).Furthermore, residential building construction employment was flat year-over-year in July, while non-residential was up by 5.9%, according to First American Economist Ksenia Potapov. Compared with pre-pandemic levels, residential building employment is up 10%, while non-residential building is up 3%.“Like June, the fastest monthly growth came from residential specialty trade contractors. This sub-sector comprises establishments whose primary activity is performing specific activities, such as pouring concrete, site preparation, plumbing, painting and electrical work,” said Potapov.Employment in the professional and business services sector and in the leisure and hospitality sector changed little in July.What’s next ?At the July Fed meeting, the FOMC hiked the benchmark rate by a quarter percentage point, as widely expected. During the press conference that followed the meeting, Fed Chair Jerome Powell said that another rate hike in September is “certainly possible,” but so is a pause.According to Realtor.com‘s chief economist Danielle Hale, today’s report is unlikely to sway the Fed.“Today’s jobs report is unlikely to change those odds significantly as it is one of several pieces of additional data that the Fed will have to consider before the next decision. The Fed will see not only an additional jobs report, but also two more readings each on consumer prices and producer prices along with several other indicators before its September 19-20 meeting and decision,” said Hale.On the housing market, she said that conditions are still favorable for households, supporting housing demand. However, climbing mortgage rates remain a substantial obstacle for homebuyers. Hale expects more “coping strategies” on the buyer’s end, such as moving further away to find affordability. Another outcome will be that affordable markets, such as those in the Midwest, will continue to see an outsized level of housing activity for both homeowners and renters, she said.As existing homeowners remain rate-locked into their homes with no financial incentive to move, homeowners are likely to increasingly turn to renovating their homes to suit their evolving needs, added Potapov.

Read More$30 Million L.A. Mansion Looks Over A Secret Body Of Water

The Bel-Air property was once owned by the late Ursula Theiss, a German actress and second wife of Hollywood actor Robert Taylor.

Read MoreThis $30 Million Bel-Air Mansion Overlooks A Secret Body Of Water

The Bel-Air property was once owned by the late Ursula Theiss, a German actress and second wife of Hollywood actor Robert Taylor.

Read MoreeXp makes a $9.4M profit in Q2 despite headwinds

eXp World Holdings faced headwinds in the second quarter, as persistently slow real estate sales drove the company’s revenue down 13% year-over-year to $1.2 billion, executives disclosed on Thursday.Despite the decline in revenue, the holding company for eXp Realty maintained profitability with a net income of $9.4 million, up from $1.5 million in the first quarter of 2023 and $9.3 million in Q2 2022.The company’s adjusted operating earnings before interest taxes depreciation and amortization (EBITDA) declined 15% year-over-year to $38.1 million in Q2 2023, according to the official statement. Amid a difficult housing market, transaction sides declined 9% to 137,199. Sales volume also declined 16% from the second quarter of 2022 to $48.6 billion.However, eXp World Holdings Chief Executive Officer Glenn Sanford expressed his satisfaction in spite of the declines in revenue, sales and transactions. The company and its subsidiaries, which include eXp Realty, SUCCESS Enterprises, Virbela and other affiliated services, are in solid financial shape, declared its executives. “Our net income and adjusted EBITDA were both positive, we continue to have a solid financial profile, we have a strong cash flow generation and a significant cash balance as well as zero debt,” said Sanford during the company’s webcast. International Realty was the best performing segment in Q2When broken down by segments, International Realty revenues increased 35% year-over-year to $11.99 million, reaching an all-time record. North American Realty revenues, on the other hand, fell by 13% year-over-year to $1.21 billion.“North American Realty business continues to be strong and profitable with unit growth and agent growth outperforming the industry. It delivered $34 million of EBITDA in the quarter,” said Sanford. Jeff Whiteside, CFO and Chief Collaboration Officer of eXp World Holdings, acknowledged that high mortgage rates were expected to persist in the short term. However, he stated that consumer price inflation started to cool down in the U.S, eXp’s core North American market.He further noted that “forward interest rate curves suggest that rates may now be at or near peak levels.”As such: “We are optimistic that lower mortgage rates will unleash significant pent-up demand as affordability improves and buyers can once again meet seller price objectives.” The company remains bullish on iterating its agent value propositionDuring the webcast Thursday, Sanford touted eXp Realty’s growing value proposition among agents, pointing to a 7% increase in agent count to 88,248 as of June 30, 2023. Just yesterday, Daryl Owen, the founder of top California independent brokerage Nationwide Real Estate Executives, joined eXp Realty, taking 200 agents along with him. Sanford highlighted the launch of several initiatives in Q2 that prioritize agent support. The brokerage revamped its eXpert Care Desk, which provides live support to agents 24/7. And in May, they launched Luna, the GPT-4 powered generative AI support agent.Throughout the second quarter, eXp also made a series of notable announcements, including the launch of its Boost Program to financially incentivize independent teams and brokerages to join eXp Realty and its commitment to reduce its revenue share criteria.

Read MoreOpendoor delivers profitability, buys 2,680 homes in Q2

Opendoor continued to feel the market’s headwinds in the second quarter of 2023, which led to fewer homes sold and lower revenues in the period. But the iBuyer greatly reduced its operating costs, delivered a profit, and increased its home purchases in the quarter. The iBuyer recorded a net income of $23 million from April to June, compared to a net loss of $101 million in the previous quarter and a net loss of $54 million in the same quarter last year, per Securities and Exchange Commission (SEC) filings. The firm’s revenues came in at $2 billion in the second quarter of 2023, down 37% compared to the previous quarter and 53% related to 2Q 2022. Total operating expenses declined to $217 million, compared to $294 million in Q1 2023 and $454 million in Q2 2022. Carrie Wheeler, CEO of Opendoor, said the company exceeded the high end of its guidance for adjusted Ebitda and revenues in the second quarter as it continues to “focus on what we can control and operate with discipline in this environment.” In April, the iBuyer announced that it had made the “very difficult decision” to lay off roughly 22% of its workforce, or 560 positions. More layoffs followed in November 2022, when Opendoor cut 550 jobs, or approximately 18% of its workforce at the time.“Our results reflect the progress we’ve made in strengthening our offering, driving cost efficiencies and managing risk. We expect the third quarter to mark our return to positive contribution margin levels,” Wheeler said in a statement. Opendoor has committed to deliver at least 100 basis points of contribution margin improvement by 2024, increasing the annual target range to 5% to 7%, with a goal of eventually returning to positive adjusted net income. The contribution margin was negative 4.6% in Q2 2023. “We expect to perform within our 5% to 7% contribution margin target beginning Q4 2023,” Opendoor’s interim CFO Christy Schwartz told analysts Thursday. “We are managing our business to return to positive adjusted net income, which is our best proxy for operating cash flow. And we believe we have the cost structure and balance sheet in place to do so.” Schwartz said the company expects to reach breakeven at steady annual revenues of $10 billion, or approximately 2,200 home acquisitions and resales per month at its target contribution margin range of 5% to 7%. But what about selling and buying homes? In the second quarter of 2023, Opendoor sold 5,383 homes, a decline of 35% compared to 1Q 2023 and 49% compared to 2Q 2022. “As of quarter end, 99% of the homes we made offers on between March and June of last year were sold or under resale contract and our new book of inventory is generating positive unit economics in what continues to be an uncertain time in the U.S. housing market,” Wheeler said. Meanwhile, Opendoor’s inventory balance reached $1.1 billion in the quarter, representing 3,558 homes. The total is down 46% from the previous quarter and 83% from the same period last year. The company purchased 2,680 homes from April to June, up 53% from Q1 2023 and down 81% from Q2 2022. The decline versus the prior year comes primarily from elevated spreads embedded in its offers since June last year, coupled with sellers remaining on the sidelines, Opendoor’s executives told analysts. Opendoor ended the quarter with 1,390 homes under contract for purchase, up 22% versus Q1 2023.Looking forward, the company expects to deliver revenues between $950 million and $1 billion in Q3 2023 when adjusted Ebitda is expected to be between negative $60 million and $70 million. The firm is optimistic about the opportunities it has cultivated, including its partnership with Zillow and its Opendoor Exclusives platform.

Read MoreRocket has a profitable quarter and a new CEO

Rocket Companies, the parent of Rocket Mortgage, returned to profitability in the second quarter of 2023 driven by an increase in the purchase mortgage market share and expense cuts in business lines that aren’t profitable. The Detroit-headquartered lender’s GAAP net income in Q2 was $139 million, an improvement from GAAP net loss of $411 million in 2023 Q1. Rocket posted a $33 million adjusted net income loss in the second quarter, following a $111 million loss in Q1. Rocket is “very pleased to see our purchase market share grow on both a year-over-year and quarter-over-quarter basis. Our focus on servicing clients through innovation in this challenging market is working,” Bill Emerson, interim CEO of Rocket Companies, told analysts in its earnings call.Rocket generated $22.3 billion in origination volume in Q2, up about 31% from $17 billion in Q1 2023. The second quarter production represents a 35% drop compared to the same period in 2022. Gain-on-sale margins posted for the second quarter of 2023 was 267 points, up from the previous quarter’s 239 points. By channel, Rocket reported $12.4 billion in sold loans through its direct-to-consumer channel and $9.6 billion through its TPO channel, its conduit to mortgage brokers and historically a stronger source of purchase business. The company doesn’t break out purchase business versus refinancings in its earnings reports.“We’ve seen growth in both channels. It’s not specific or exclusive to one or the other and we’re actually happy about the growth in both,” Emerson said to an analyst asking where the purchase market share gains came from. Rocket’s share of the purchase business jumped to 55% in the first three months of 2023, according to data from Inside Mortgage Finance (IMF). Purchase volume in the first quarter came in at $9.4 billion, ranking third in the IMF’s rankings.Rocket’s strategy going forward will remain the same – pursuing its direct-to-consumer business and TPO channel, Emerson noted. HousingWire recently published a deep-dive feature on whether Rocket’s accelerated efforts of hiring local loan officers represented a shift in the lender’s strategy.“As we look at our direct-to-consumer business, there’s a way to get more local and more regional with that out of a centralized location that I think is beneficial to the interactions that we would have with realtors and builders, and that’s something that we’re constantly working on and evaluating, but I think what you’re seeing is an organization that’s committed to a direct-to-consumer model, the digitization of the process,” Emerson said.Betting big on fintechRocket has been betting big on the strength of its platform — branding itself as a fintech. With Varun Krishna — a veteran in the financial technology world who held executive positions at Intuit and PayPal — taking helm of the company as CEO starting in September, Rocket has its vision set on growing its platform.“He (Varun) clearly rose to the top as far as someone that would be able to come in here and paint a great strategic vision for the organization, someone who had alignment with us in a fintech space and the abilities that we have and the things that we’re looking to do as it relates to expanding our business and our platform and our ecosystem,” Emerson said.The number of Rocket accounts grew to 29.3 million, an increase of nearly 2 million, as of June 30.Rocket reiterated its priority of diversifying client acquisition channels, lowering client acquisition costs and engaging clients through their lifetime — lifting conversion from lead to close. Financials Rocket focused on operational efficiency and trimmed its cost structure through voluntary buyouts and winding down businesses that were not profitable.In July, Rocket offered its third round of voluntary buyouts to employees. Its previous two rounds of buyouts resulted in a staff reduction of about 30% in 2022.A one-time charge of about $50 million related to the voluntary career transition program primarily in Q3. The company pivoted from investing in a sales platform for solar to only offering solar financing through the Rocket Loans platform; and shut down operations of Rocket Auto — measures which are expected to save costs between $150 million and $200 million on an annualized basis. The company’s expenses were $1.1 billion in the second quarter, remaining flat from the previous quarter’s $1.1 billion. Net revenue for Q2 came in at $1.2 billion, nearly doubling from $666 million in the previous quarter. Revenue in Q2 2022 was $1.4 billion.Rocket’s liquidity improved in Q2 to $8.6 billion from $8.1 billion from the previous quarter.The Detroit-based lender closed the second quarter with $900 million cash-on-hand and $6.4 billion of mortgage servicing rights. Rocket’s mortgage servicing portfolio included more than 2.4 million loans service, with approximately $500 billion in unpaid principal balance. The lender generated $343 million of cash revenue from its servicing book, which represents approximately $1.4 billion on an annualized basis. What’s ahead for Q3? A third of the way into Q3, Rocket sees purchase mortgage shares growing but the lack of inventory will continue to be a challenge. “The trends are very consistent, particularly on the purchase side with what we saw in Q2. So that’s the good news. The challenge comes back to the inventory levels,” Brian Brown, CFO said in the earnings call. Rocket is focused on bringing in origination volume from existing homes on the market.“While we are always encouraged by a little bit of increase in the new construction, it’s still relatively small in the grand scheme (…) We are constantly working with builders on that, but that’s not going to show any short-term positive impact for us from a closed loan perspective along the line,” Emerson told analysts. Rocket expects to post an adjusted revenue between $850 million to $1 billion in Q3.

Read MoreBranden Lopez promoted to General Counsel at @properties

@properties announced the promotion of Branden Lopez to the position of General Counsel. This move comes as @properties aims to expand its business and enhance legal support across its portfolio of enterprises.Lopez, who joined @properties in November 2022 as Director of Legal, has proven herself as a key member of the leadership team for @properties and Christie’s International Real Estate. In her new role, she will be responsible for overseeing various legal aspects of @properties’ fast-growing business.Branden LopezAs the second-largest privately held brokerage firm in the United States, @properties boasts an impressive array of businesses under its umbrella, including the renowned Christie’s International Real Estate global luxury brand, the @properties franchise brand, multi-state title company Proper Title, and other real estate ventures.@properties was ranked No. 8 by both transaction sides and sales volume in the 2023 RealTrends 500 brokerage rankings. Among her core duties, Lopez will handle legal matters related to affiliate agreements in the U.S. and internationally for both @properties and Christie’s International Real Estate. Additionally, she will ensure compliance with local licensing laws and General Data Protection Regulation (GDPR) laws concerning marketing in Europe. The management of outside counsel and the protection of @properties’ intellectual property portfolio will also fall under her purview.Lopez brings extensive expertise to her new role, with more than 17 years of experience as a corporate attorney, including 15 years in the real estate industry. She is a member of esteemed professional organizations such as the Florida Bar Association, the D.C. Bar Association, the Commercial Real Estate Women Network (CREW), and the International Council of Shopping Centers (ICSC). Lopez holds an undergraduate degree from Florida State University and a J.D. from the Stetson University College of Law.

Read MoreHomeServices appeal rejected as October commission trial looms

An October trial in federal court for one of the many commission lawsuits is imminent after HomeServices of America lost a recent appeal. The 8th Circuit Court of Appeals’ three-judge panel concurred with a lower district court’s decision that HomeServices is not permitted to enforce arbitration agreements signed by seller clients of franchisees under its authority.Earlier this year, the defendants filed a motion to compel the plaintiffs into arbitration rather than have the court decide the case, but this motion was denied by Judge Stephen R. Bough of U.S. District Court in Western Missouri in July. In response, HomeServices and its subsidiaries appealed the decision to the U.S. Court of Appeals for the Eighth Circuit. The recent ruling agreed with the lower court’s opinion, noting, “HomeServices is neither a party nor a third-party beneficiary of the Listing Agreements or the Arbitration Agreements.”Lawsuit scheduled to go to courtThe case, known as Sitzer/Burnett, named after the lead plaintiff, is scheduled to go to court October 16 in Missouri. Judge Bough will make a final decision about that date at a scheduled September 9 pretrial hearing.Originally filed in 2019, the lawsuit won class-action status shortly after, and alleges that some NAR rules, including one that requires listing brokers to offer buyers’ brokers a commission in order to list a property in a Realtor-affiliated MLS, violate the Sherman Antitrust Act by inflating seller costs.Through the class certification, hundreds of thousands of home sellers in four MLS markets in Missouri can ask the defendants, which include Keller Williams, RE/MAX, HomeServices of America and its subsidiaries BHH Affiliates and HSF Affiliates, as well as Anywhere (referred to as Realogy in the lawsuit) and NAR, to be reimbursed for the $1.3 billion in commissions they paid to buyers’ agents in the past eight years. However, potential treble damages could put the total damages in the case at around $4 billion.MLSs under the gunReal estate commissions have been scrutinized by The Department of Justice and multiple lawsuits concerning how buyers’ brokers get paid are in various stages. Last month, as reported by HW Media Real Estate Reporter Brooklee Han, the nation’s second largest multiple listing service, Bright MLS, will begin allowing listing agents to put in a blanket offer of compensation for buyer brokers of zero dollars or more, starting on August 9.This change appears to possibly diverge from a National Association of Realtors rule, which states that listing agents must make an offer of cooperative compensation to buyers’ brokers in order to list a property on the MLS.Then, after years of litigation, in July, New England’s largest multiple listing service (MLS) signed off on a settlement agreement that would force it to pay $3 million, overhaul its policies and cooperate against the remaining real estate franchisor defendants in the suit.The other defendants in the lawsuit, known as Nosalek after its lead plaintiff, include Anywhere, RE/MAX, Keller Williams and HomeServices of America.Originally filed in December 2020, the lawsuit alleges that the broker-owned MLS Property Information Network (MLS PIN) is not directly required to abide by the National Association of Realtors (NAR) rules. However, it has nonetheless adopted a rule similar to an NAR rule requiring listing brokers to offer a blanket, unilateral offer of compensation to buyer brokers in order to submit a listing to MLS PIN.According to the proposed agreement, the brokers who own MLS PIN will be covered by the settlement unless they are defendants in the lawsuit. MLS PIN has 46,000 subscribers throughout New England and New York, as well as a staff of 60 employees.

Read MoreBlack Knight reports slimmer Q2 profit ahead of trial on ICE deal

Black Knight reported slimmer profits and slowing organic growth in the second quarter, largely due to weaker mortgage volume from clients as well as near-term effects from the proposed merger deal with Intercontinental Exchange (ICE).The company’s profit dropped 61% quarter over quarter to $55.3 million in Q2 2023. Profit rose 32% from $40.3 million in Q1 2023. “Our second quarter results reflect a weaker than expected mortgage market coupled with the near-term effects of the proposed merger with ICE. Revenue declined 4% on an organic basis driven by lower origination volumes as well as indirect effects of the mortgage market on our originations software business,” Black Knight CEO Joe Nackashi said in a statement.Black Knight’s revenue in the second quarter reached $368.2 million, declining 7% from the same period in 2022.“High interest rates following the rapid rise since early 2022 continue to cause operational challenges for Black Knight’s clients and prospects,” the company noted in its 8K filing.Heightened focus on expenses by clients and prospects, as well as the proposed ICE transaction, has elongated the sales cycles in the short term; market conditions continue to result in elevated originator consolidation, bankruptcies and associated attrition, according to its filing with the Securities and Exchange Commission (SEC). Software solutions represented 87.9% of the revenues in the first quarter, with an operating margin of 41.4%, down from 45.6% in the same period of 2022. “Our origination software solutions revenues decreased $15.6 million, or 13%, as revenues from new clients were more than offset by a decrease of $8.3 million in license fees and the effect of lower origination volumes and attrition,” according to the company’s 10 Q filing with the SEC. The remaining revenue came from data and analytics, a segment with an operating margin of 15.2% from April to June, compared to 24.9% in the previous year. Development on ICE-Black Knight merger With ICE’s proposed acquisition of Black Knight under review by the Federal Trade Commission (FTC), the two companies and the FTC are expecting a preliminary injunction hearing scheduled for August 14 – August 18. Black Knight, ICE and the FTC asked for a delay as the planned sale of Optimal Blue in July requires time for the FTC staff to analyze the implications of the divestiture and discuss a potential resolution of the pending matter.ICE and Black Knight also announced an agreement to sell loan origination system Empower to a subsidiary of Canada’s Constellation Software in March to quell FTC’s antitrust concerns. Following ICE and Black Knight’s announcement of an agreement to sell Optimal Blue, Keefe, Bruyette & Woods (KBW) noted that the divestiture of Black Knight’s Optimal Blue leaves the FTC with a weak case as it remedies the remaining horizontal overlap cited in the FTC’s complaint.KBW had floated the possibility of the FTC settling on the ICE-BK merger deal before the August 14 trial, allowing the deal to close Q3 2023.“As this case continues to evolve, it is not possible to reasonably estimate the probability that the parties will ultimately reach settlement or that the FTC will ultimately prevail on its claims. Should the parties not reach a settlement, we intend to vigorously defend against the claims of the FTC,” Black Knight’s 10 Q filing said. Due to the transaction with ICE, Black Knight has suspended the practice of providing forward-looking guidance.

Read MoreHUD Secretary tackles appraisal bias with NAREB partnership

Secretary of the U.S. Department of Housing and Urban Development (HUD) Marcia Fudge “fired up” the crowd during her keynote speech at the 2023 National Association of Real Estate Brokers (NAREB) Annual Conference when she spoke about the recently-announced HUD-NAREB partnership designed to tackle appraisal bias. “HUD and NAREB will work together to fight appraisal bias in the Black community,” Fudge said. “I live in a Black neighborhood by choice; my home is bigger, my lot is bigger, yet my home is valued less than the white neighborhood down the block; this must change.”In an announcement, NAREB described Fudge’s speech as a “dynamic and inspirational address that ignited passion and commitment among attendees at NAREB’s annual convention.”Fudge and NAREB President Lydia Pope both hail from the Cleveland, Ohio area. Fudge praised Pope’s work as the association’s leader during her speech. Fudge also addressed her commitment as HUD Secretary in addressing disparities for marginalized communities.Fudge also addressed the access to credit for borrowers of color, and discussed the work HUD and the Biden administration are doing to address the role homeownership plays in building generational wealth, a common point of discussion for HUD under her leadership thus far.“Some Black borrowers lack credit, but now when obtaining an FHA loan, rental history can be used as a credit history,” she said, touching on recent policy changes at HUD and the Federal Housing Finance Agency (FHFA) that considers on-time rent payments as a part of a potential borrower’s credit history.In terms of the role homeownership takes in building wealth for families, Fudge reiterated her belief in forging a more direct path to homeownership. “We cannot deal with inflation until we deal with the housing crisis,” she said. “Most of us build wealth through homeownership.”Fudge also admonished certain policymakers for telling younger people that they don’t need to own a home.“Who told them that foolishness?,” she reportedly asked rhetorically. “We need to help get them in homes, so we need your advocacy. […] Stay encouraged, stay vigilant, We need you. Thank you,” she concluded.

Read MoreMortgage rates tilt towards 7% as the 10-year treasury yield jumps

Mortgage rates continued to inch towards 7% this week as the 10-year treasury yields climbed past the 4% threshold.Investors assessed the state of the U.S. economy after Fitch Ratings downgraded the U.S.′ long-term, foreign currency issuer default rating from AAA to AA+ on Tuesday. The following day, the U.S. Treasury announced that it would sell off more than $100 billion of long-term securities. Some economists say that this development contributed to drive up the 10-year treasury yield to its highest level since November 2022. However, there are differing opinions on this matter. According to HousingWire’s analyst Logan Mohtashami, the stronger labor data had a bigger impact on mortgage rates and the bond market than the sale of long-term securities or the default rating.Freddie Mac’s Primary Mortgage Market Survey, which focuses on conventional and conforming loans with a 20% down payment, shows the 30-year fixed rate averaged 6.90% as of August 3, up from last week’s 6.81%. By contrast, the 30-year fixed-rate mortgage was at 4.99% a year ago at this time. The 15-year fixed-rate mortgage also rose this week to 6.25%, up 14 basis points from the prior week.“The combination of upbeat economic data and the U.S. government credit rating downgrade caused mortgage rates to rise this week,” said Sam Khater, Freddie Mac’s chief economist. “Despite higher rates and lower purchase demand, home prices have increased due to very low unsold inventory.”The sudden hike of the 10-year Treasury, along with upcoming employment and inflation data, will influence how much mortgage rates may rise in the short term, economists say. If employment and inflation pick up steam, mortgage rates are likely to continue climbing as markets prepare for further monetary tightening, said Realtor.com Economic Data Analyst Hannah Jones. On the bright side, the prospect of a recession is dimming for the next six to 12 months.Other mortgage rate indices showed mixed results on Thursday morning: HousingWire’s Mortgage Rates Center showed Optimal Blue’s 30-year fixed rate for conventional loans at 7.02% on Wednesday, compared to 6.85% the previous week. At Mortgage News Daily on Thursday morning, the 30-year fixed rate for conventional loans was at 7.20%, up 25 basis points from the previous week.The economy remains on firm footingRegarding the housing market, new economic data further solidify the view that the economy remains on firm footing, highlighted George Ratiu, chief economist at Keeping Current Matters.“Construction spending advanced in June, a sign that companies and the government continue investing in real estate and infrastructure projects. Meanwhile, the number of open jobs retreated slightly, but remained above 9 million, while the number of workers leaving their positions for better ones remained elevated. Many companies still deal with a shortage of labor, as evidenced by the private payroll data which outpaced market expectations,” said Ratiu in a statement. Look for payroll employment data tomorrow“Tomorrow’s government report on payroll employment will add another data point to the bigger picture, with economists looking for changes in the unemployment rate and wage figures,” he added.Meanwhile, active inventory fell compared to the previous year each week in July as many homeowners held off on listing their home for sale, noted Realtor.com Economist Jones.“The drop in for-sale inventory was met with the typical seasonal pick-up in buyer demand, despite affordability constraints, which propped up home prices. In the second quarter of 2023, homeowner vacancy fell to a historical low of 0.7% as many homeowners stayed put and home shoppers snapped up available inventory, leaving fewer homes vacant,” she said. This gap between supply and demand, exacerbated by a decade of under building, pushes prices up. Consequently, it also brings back market competition, especially in more affordable metro areas. Scarce inventory leads to a modest pace of sales for existing homes. On the new home front, growing options and more approachable prices have led to a pickup in sales transactions.Lastly, Ratiu added that mortgage rates are expected to remain elevated for the next couple of months, keeping pressure on affordability. “For buyers who are not in a hurry, the fall and winter months could bring better values and a less competitive environment to find the right home,” Ratiu concluded.

Read MoreLamacchia Realty announces mergers, enters Cape Cod market

Lamacchia Realty recently announces two significant mergers, marking an expansion for the company. Firstly, they are joining forces with Right Choice Real Estate, a well-known legacy brokerage in Massachusetts and Rhode Island for over 25 years. Founders Ron and Dawn Rusin will remain actively involved in running the office while focusing more on growing their real estate sales businesses as Lamacchia Realty takes charge of management-related tasks.Lamacchia Realty is also partnering with Foley Real Estate and Foley Premier Properties, a brokerage in Falmouth, Cape Cod. Founded in 1970 by Jim Foley, the company has been family-owned and operated ever since, with Kara Foley leading the way since 2010. This merger will see Lamacchia Realty handling most of the Cape Cod business, particularly in Falmouth, in-house.Lamacchia Realty was named a RealTrends GameChanger in 2022 and 2023 for its growth. In 2023, the firm grew by 216% by five-year transaction side percentage. The firm is also ranked in the 2023 RealTrends The Thousand No. 68 in the private independent category.The integration of these two brokerages into Lamacchia Realty’s portfolio expands their reach in both the Bristol County and Cape Cod markets. As part of the integration, the current Right Choice Real Estate office in Fall River will now operate under the Lamacchia Realty banner. The move will also expand Lamacchia Realty’s reach into the Rhode Island market.

Read More

Categories

Recent Posts