Real estate agents: Service clients with an eye on future economy

The Fed recently announced yet another interest rate hike, making borrowing more expensive and pushing the prospect of purchasing a new home out of reach for an even greater share of Americans. At the same time, inflation is easing and the economy is showing unanticipated strength, with strong employment numbers and greater than expected GDP. All this means one thing for current and prospective homeowners – they shouldn’t expect the Fed to begin lowering rates any time soon. Though this would typically signal a time for panic across the residential real estate profession, those who can focus on servicing their clients with a mind for the future will be well positioned for whenever the economics for home buying become more favorable. Double down on relationship buildingHigh mortgage rates mean those on the margins of potential homeownership are moved one step further away from their goal. It also means those currently in homes — some of whom purchased or refinanced through the historical low interest rate period after the pandemic — are disincentivized to buy a new home at current rates. Furthermore, for those looking for their next home, higher interest rates effectively reduce their buying power, translating literally to fewer and fewer square feet, bedrooms and bathrooms. Real estate teams may lament homeowners’ waning interest in buying (or selling) into this market. But there are things real estate pros can do to make productive use of the moment, and double down on relationship building with new and existing clientele.Educate and updateStay connected. One of the biggest mistakes real estate professionals can make, regardless of the market, is not staying in touch with clients. Real estate can be a transient profession with many newcomers flocking to the industry when times are good, and falling out when times are tough. Times are decidedly difficult right now, reducing deal flow and overall revenue potential. Many will see the moment worthy of a pullback in their efforts, focusing on clients with a greater, real or perceived, likelihood of being able to transact. That state of mind is an absolute mistake.Provide clients with market updates. Sharing recent news and its practical implications with current and prospective clients is an excellent way to check in and ensure they have a strong understanding of what impact rate increases, strong economic numbers and more will have on their immediate transaction prospects. Whether buying or selling a home, real estate pros who help their client base to have a clear understanding of what is happening, why, and what impact it will have, take advantage of a unique trust building opportunity. They provide clients with extra reassurance that they are indeed receiving good counsel on their (eventual) property endeavors.Track and report on falling prices. High mortgage rates hurt home buying and selling prospects. However, for some, higher interest rates can bring home prices down just enough to account for the added cost of a higher interest rate. In some scenarios, if a prospective buyer can carry a more expensive rate, they may secure a home at a lower price, and then aim to refinance when rates have improved. Understanding and activating home equity. Hikes in interest rates also affect the price of revolving debt. Most, if not all, revolving credit moves with the prime rate; meaning, it just got even more expensive to carry a balance from one month to the next. Real estate professionals can educate clients on the prospect of leveraging the equity they have in their current home to consolidate consumer debt through home equity based products like HELOCs, home equity loans or other home equity based products, that tend to have better terms than other forms of debt. Home-equity products also provide a path to financing home improvement projects that can raise the value of a home, while clients wait for the environment for putting a home on sale to improve. Keep the door open. Financial situations are constantly in flux. Did a client recently get a new job? Did a relative pass away leaving them with a large inheritance? Did your clients just become empty nesters? New occurrences in life bring about different new ways to view possibilities. No one wants to buy a home for more money than they have to, but new circumstances can open the door to revisiting property aspirations that weren’t reasonable conversations just moments before. Keeping an open door to those who have new circumstances will help real estate pros adjust their approach for specific clients. Unprecedented and unfamiliar economic cycles like the one we are in today provide a great deal of room to drop the ball or lose interest. Those real estate teams that refocus on the basics of building trust through credible counsel and insight will see more deeply engaged client prospects, and eventually, transactions that can keep the business afloat during a time when the entire industry is facing headwinds. Jeff Levinsohn is CEO and Co-Founder of House Numbers, a service to help homeowners gain financial independence by understanding and optimizing their largest asset — their home.

Read MoreFannie Mae scraps title waiver pilot program

The American Land Title Association (ALTA) is celebrating a huge win in its ongoing war against title insurance alternatives. Fannie Mae is no longer considering a pilot program that would bypass traditional title insurance by granting certain mortgage lenders a waiver on title insurance requirements for loans sold to Fannie, according to an announcement earlier this month.This is a major victory for the trade group, which felt that Fannie Mae was “moving beyond its charter” with this pilot program.News of the rumored pilot program came in March, roughly a year after Fannie Mae first announced that it would be accepting attorney opinion letters (AOLs) in lieu of title insurance in limited circumstances.The pilot program was said to have been a component of the government sponsored entities’ (GSEs) Equitable Housing Finance Plans, which are required by their regulator Federal Housing Finance Agency (FHFA).The initial version of the GSE’s Equitable Housing Finance Plans were approved in the summer of 2022 by the FHFA.“The intent was to promote affordable and sustainable housing opportunities for more households nationwide,” Diane Tomb, the CEO of ALTA, told HousingWire late last year. “One of the goals they outlined in those plans is a push to reduce closing costs, especially for low-income borrowers. Based on those plans, both GSEs are pushing pilot programs promoting the use of attorney opinion letters, reportedly as an alternative to reduce closing costs.”According to an email Tomb sent to ALTA members earlier this month, obtained by HousingWire, more than 200 trade organization members shared their concerns about the title waiver pilot program with members of Congress.“This is a significant achievement to protect consumers, lenders and the housing finance system, and showcases the benefits of our products, industry and your business. The success of challenging this pilot underscores the value of advocacy and making your voice heard,” Tomb wrote in the email. “Importantly, we will continue to work with the FHFA and policymakers to thoughtfully address housing affordability and opportunity. We will also continue to collaborate with Fannie Mae and Freddie Mac to deliver innovative and cost-effective title insurance products and solutions that best protect lenders and consumers.”Despite scrapping this pilot program, Fannie Mae said it will continue to look for ways to improve housing affordability.“Housing affordability is key to Fannie Mae’s mission, and we remain committed to our ongoing engagement with industry partners and providers to explore ways to make the homebuying process more affordable and accessible in a manner that does not increase risk for borrowers, lenders, and the marketplace,” a Fannie Mae spokesperson wrote in an email.For its part, ALTA said it is working on lowering closing costs where it can, and it believes the increase in automation and improved technological capabilities within the title industry will lower costs over the next few years.“Over the last 10 years, rates have gone down 6% across the industry and that is important for homeowners and it’s because of the investment the industry has put into things around automation and using machine learning and AI to search title and come to a faster decision about the title,” Steve Gottheim, ALTA’s general counsel, told HousingWire last November. “These technologies come with a cost at the front end, but over time, they bring that efficiency and bring the price down.”During the first quarter of 2023, title insurers brought in $3.37 billion in title insurance premiums, while paying out just $162.7 million in claims during that same time period, according to data from ALTA.

Read MoreWeWork On The Rocks Again – What Comes Next

Looking ahead, if WeWork does actually close the adverse impact on landlords could be significant if its leases are not picked up by another co-working operator or sev...

Read MoreDubai’s Jumeirah Islands Welcomes A New Resident: Telegram’s Billionaire Founder

Telegram founder Pavel Durov is renting a new pad in the emirate’s ritzy neighborhood.

Read MoreJohn’s Island, Florida, Estate Offers A Lifestyle For The Super-Rich

With asking prices that can reach upward of $20 million, the island’s gated estates offer a lifestyle that appeals to a highly elite and exclusive clientele, says Troy...

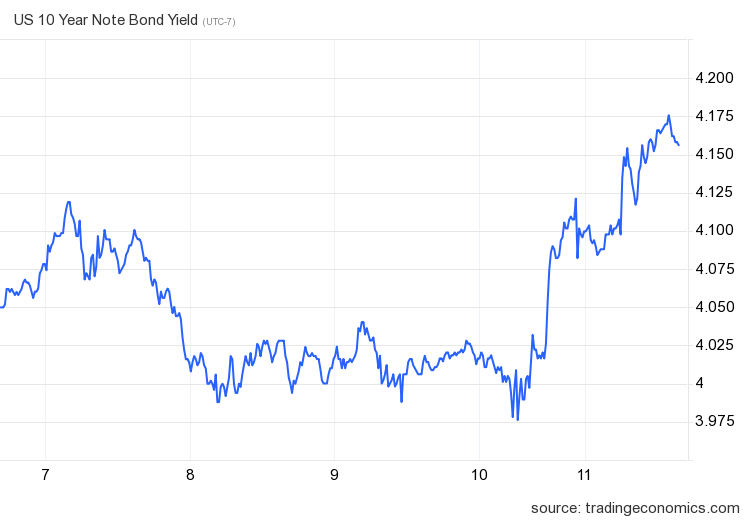

Read MoreWhere are mortgage rates headed?

Last week ended with a wild ride for mortgage rates. We anticipated the two inflation reports could help mortgage rates, however, we had a bad bond auction last Thursday, and the 10-year yield rose sharply. Weekly active inventory grew slowly again and purchase apps were down week to week again.Weekly active listings rose by only 4,270Mortgage rates went from 7.03% to 7.19%Purchase apps were down 3% week to weekMortgage rates and bond yieldsLast week we started with lower bond yields as we anticipated inflation reports to continue the trend of slower year-over-year inflation data. This happened as expected, except we had a lousy bond auction, which meant too much debt supply came online with insufficient buyers. This pushed yields higher Thursday and Friday to move mortgage rates to 7.19%.A valid case for higher mortgage rates in the short term is that we are simply going to be in an environment where we don’t have a lot of bond buyers versus the supply coming in, thus making it harder for mortgage rates to go lower. We saw an example of that last week. For my 2023 forecast, my range on the 10-year yield has been between 3.21%-4.25%, emphasizing that the bond yields can go lower than 3.21% only if the labor market breaks. The labor market breaking to me is if jobless claims on a four-week moving average go over 323,000; currently, that data is 231,000. As the economy has stayed firm, bond yields are at a higher level of my range for 2023.Weekly housing inventoryThe painful housing inventory story of 2023 continues as we had yet another week of slow inventory growth. Last year when mortgage rates spiked higher, inventory growth was much faster, but we were also working from the lowest levels recorded in history in March of 2022. This year, it’s been a much different story. Weekly inventory change (August 4-August 11): Inventory rose from 487,870 to 492,140Same week last year (August 5-August 12): Inventory rose from 543,898 to 550,175The inventory bottom for 2022 was 240,194The inventory peak for 2023 so far is 492,140For context, active listings for this week in 2015 were 1,203,577As we can see in the chart below, inventory growth has been so slow that active listings have been negative year over year for some time now. For those calling for a massive inventory spike since 2008, the last few years have not gone as planned.New listings data has been trending at the lowest levels recorded in history for more than 12 months. However, even with higher mortgage rates in the last few months, we haven’t seen a new leg lower in this data line, which means we might be forming a workable bottom in 2023. As you can see in the chart below, 2023 has had a clear divergence versus 2021 and 2022 data, which were already at all-time lows before last year.Here’s how new listings this week compare to the same week in past years:2023: 60,7592022: 73,3842021: 79,184Purchase application dataPurchase application data was down again by 3% last week, making the count year-to-date at 14 positive and 16 negative prints. If we start from Nov. 9, 2022, it’s been 21 positive prints versus 16 negative prints. Mortgage rates near or above 7% are simply too high to promote real growth in this data line, which is working from a historical bottom. So, when rates fall, moving the needle higher for purchase apps won’t take much. However, for now, rates this high have facilitated more negative week-to-week data than positive, leading to lower sales as this data line looks out 30-90 days. While we aren’t seeing sales collapse like last year, we aren’t growing sales meaningfully from the recent lows. The week ahead: Tons of economic dataThis week, we have various economic data reports that can move mortgage rates and give us a sense of where the housing market is going. Retail sales and the Leading Economic Index are out this week. Also, we get two key data lines for housing this week: the homebuilders survey by NAHB/Wells Fargo and housing starts! What I am looking for in housing data is what the builder survey indicates for the next six months. In last month’s report, we saw a slight decline in this data line. For this week, I want to see how mortgage rates react to the batch of new economic data.

Read MoreWhat Do Accredited Investors Need To Know About Crowdfunding Today?

While some crowdfunding platforms are available to all investors, others require individuals to meet certain criteria to participate.

Read MoreCenturies-Old Coach House Offers City-Close Country Living Near London

Set on a walled half-acre site, the historic residence is just outside central London in the village of East Sheen.

Read MoreMillion-dollar homes nearing 10% of market as property prices rise

Nearly one in ten homes in the U.S. are worth at least $1 million dollars, close to all-time-high levels of June 2022, according to a new report from Redfin.Just over 8% of homes are worth $1 million or more, not far off the high of 8.6% in June. This upswing in home prices comes on the heels of a major dip in February, when only 7.3% hit the $1 million price threshold. Home prices are increasing on a year-over-year basis after declining at the beginning of the year. The median U.S. home-sale price rose 3% year over year in July, the biggest increase since last November. Prices are rising faster for luxury homes, with the median sale price of up 4.6% year over year to $1.2 million in the second quarter.Of course, elevated mortgage rates are symbolically handcuffing homeowners who want to cling to lower mortgage rates. As a result, inventory is scarce and homebuyers are competing for few available homes on the market. Steady demand is driving up prices, and affordability issues persist as buyers contend with high rates.The number of homes actively for sale decreased by 6.4% compared to last year, according to the July Monthly Housing Market Trends Report from Realtor.com. “In most of the country, expensive properties that are in good condition and priced fairly are attracting buyers and in some cases bidding wars, mostly because for-sale signs are few and far between right now,” says Redfin Economics Research Lead Chen Zhao. “Recent economic signals that the U.S. may avoid a broad recession could cause high-end buyers to feel more confident in making a major purchase in the coming months. There may be more demand coming down the pipeline.” Hence, “there’s no rush to offload high-value homes.”Meanwhile,, the share of homes worth seven figures has doubled from pre-pandemic levels, just over 4% of homes were valued at $1 million or more in June 2019. The share shot up when home prices skyrocketed in 2020 and 2021 as record-low mortgage rates and remote work drove Americans to buy homes.Home prices in East coast metros are rising the fastestMillion-dollar homes are increasing quickly in some parts of New England. For example, 25.8% of homes in the Bridgeport, CT metro are worth at least $1 million, up from 23.1% a year ago, the biggest increase among metros in Redfin’s analysis. Boston, where the share increased from 20.3% to 21.5%, was second, followed by Newark, NJ (8.7% to 9.7%).Nationally, the number of homes worth $1 million or more rose year over year in 55 of the 99 most populous U.S. metros. However, the uptick remains small, less than one percentage point, in almost all of those.The share of seven-figure homes is falling in West Coast metros Expensive coastal metros are losing million-dollar homes fastest. Seattle scored the biggest drop in share of expensive houses, from 39.3% to 33%. Oakland, CA (55.1% to 49%) and Oxnard, CA (40.2% to 34.5%) placed second and third, respectively.Los Angeles, San Diego, San Jose, San Francisco, Anaheim, New York and Washington, D.C. are also among the metros that saw drops in the number of million-dollar homes.Still, California has the highest share of million-dollar-plus homes in the country, by far.Million-dollar homes are rare in some parts of Texas and the Rust BeltFew million-dollar homes can be found in several inexpensive metros, including parts of Texas and upstate New York.For example, the share of homes worth $1 million or more is 0.5% or lower in Omaha, NE; Dayton, OH; McAllen, TX; El Paso, TX; Akron, OH; Detroit; Buffalo, NY; Elgin, IL and Rochester, NY.

Read MoreTrade groups oppose rent control on GSE-backed multifamily properties

A coalition of high-profile housing providers, resident and lenders’ associations say rent control could increase rent, reduce the capital to boost housing supply and hurt renters.The letter was in response to a request for input issued by the Federal Housing Finance Agency (FHFA) in May regarding protections for tenants in Fannie Mae and Freddie Mac-backed multifamily properties. It followed a Biden administration initiative launched in January urging housing providers and local governments to combat soaring rents. On Thursday, 18 associations for housing providers, lenders and residents sent a letter to the FHFA Director Sandra Thompson in which they oppose the inclusion of mandatory rent control and rent stabilization policies as a condition of the government-sponsored enterprises (GSEs) financing for multifamily properties. The group included the Mortgage Bankers Association, National Association of Home Builders, National Association of Realtors, National Multifamily Housing Council and the National Housing Conference.A February 2022 study found that 27% of firms surveyed would be willing to keep their current investments or add new ones in rent-controlled markets, the groups said in a statement, without offering further details.The FHFA said in a statement that the agency “has taken robust actions to support and promote multifamily tenant protections” and “routinely engages stakeholders, Congress, and the public regarding concerns on this critical topic.” The agency is reviewing more than 3,600 comments, the FHFA stated. The comment letter argued that rent control programs usually incentivize current renters to stay for longer periods, limiting opportunities for other prospective renters. It would be contrary to Fannie and Freddie’s mission to create more affordable housing for low and moderate-income residents, they argued.The MBA, representing lenders and servicers, said in a recent letter to the FHFA that adding tenant protections to a GSE-guaranteed mortgage is not a “workable or lasting solution.” Enterprise multifamily loans can have terms as low as five years with a balloon payment at maturity, and often borrowers pay off the loan before the end of the term. “Enacting new or expanded obligations, like rent control, would disincentivize participation in the Enterprise multifamily programs or in the overall production of affordable housing,” the MBA said in a statement. “The most effective way to help renters in need is to increase the supply of affordable housing by fully funding successful, proven programs like Section 8, Low-Income Housing Tax Credits, and more.” Manufactured housing is a concern The discussion on rent control policies, however, has its nuances. Jim Gray, a senior fellow at the Lincoln Institute of Land Policy, said rent control, in most cases, is not a solution for affordable housing problems. Among them is the recent phenomenon of “predatory investors” buying up large numbers of single-family properties and quickly imposing significant rent increases, which affected manufactured housing communities with concrete pads. “When land rents are raised unreasonably — often because the investor knows the homeowner can’t afford to move her unit — this is a very different situation than what’s addressed in most of the studies we’re aware of on rent control,” Gray said. “We think the market has changed in a way that there are circumstances where limitations on rent increases may be good public policy.” Currently, Fannie Mae and Freddie Mac finance Manufactured Housing Communities (MHCs) – where residents own their homes and lease the pad on which the house is situated – only when the owner offers protections to tenants, the FHFA said in the RFI. These protections include renewable lease terms, advance notice of rental payment increases or sale of a manufactured housing community, and rights regarding the sale of their manufactured homes. The Lincoln Institute of Land Policy also sent a letter to the FHFA, with other four organizations, including the American Council for an Energy-Efficient Economy, Housing Assistance Council, Local Initiatives Support Corporation and Prosperity Now.The group recommended that Fannie Mae and Freddie Mac explore additional options to strengthen their protections by retaining the 60-day advanced notice period for a planned sale while establishing a 180-day notice for planned closures. “We also recommend that tenants, nonprofits and public entities have the right to match any MHC purchase offer within 180 days of when an MHC with an Enterprise-backed loan is sold.” The organizations suggest that FHFA should set forth measures to prevent landlords from refusing to rent to someone because of their source of income; require notice at least 30 days before rent increases; eliminate unnecessary fees that prevent tenants from applying; and establish just-cause requirements to prohibit landlords from evicting renters for specific discriminatory reasons.A federal government push In January, the White House launched the ‘resident-centered housing challenge,’ which urged housing providers and local governments to step up their policies to protect tenants as rent prices soared. To illustrate the challenge, a recent Redfin report showed that the U.S. rental market has been slowing for over a year, but the median asking rent in June of $2,029 was not far off the record $2,053 in August 2022. According to the White House, roughly 35% of the U.S. population — or over 44 million households – live in rental housing. Nearly one-third of all rental units nationwide are financed with federally backed-mortgages. The FHFA said in its request for input that the GSEs’ responsibility is to “not only ensure liquidity is available for affordable rental housing but also to address challenges faced by tenants and property owners in the multifamily housing market.” The RFI states that the GSEs have voluntary rent restriction programs in place that preserve affordable housing. Freddie Mac offers flexible credit terms to borrowers who agree to preserve affordable rent levels on a portion of units at a multifamily property for a specified period. Meanwhile, Fannie Mae has a program that requires multifamily borrowers to restrict rents in 20% of units for tenants with incomes at or below 80% of an area median income (AMI).

Read MoreCertain CFPB enforcement actions in limbo ahead of constitutionality ruling

Certain enforcement actions being sought by the Consumer Financial Protection Bureau (CFPB) are being stayed in courts pending the outcome of an upcoming United States Supreme Court case that will decide the Bureau’s constitutionality.In a predatory lending lawsuit the CFPB and New York Attorney General filed against Credit Acceptance Corp, U.S. District Judge Jennifer Rearden cited the pending decision in Consumer Financial Protection Bureau v. Community Financial Services Association of America, Limited (CFSA) that will decide whether or not the CFPB’s funding structure is constitutional, according to reporting by Reuters.“The regulators argued that the CFPB’s funding status had no bearing on whether their lawsuit could proceed,” the reporting said. “But the judge said that while the public had an interest in seeing consumer protection laws enforced, ‘any potential harm to the public caused by delaying this action is outweighed by the benefit to consumers in proceeding in a streamlined fashion.’”The judge also argued that a stay in the decision is prudent since the Supreme Court case “could contain guidance that would allow this litigation to proceed on a reasonable and efficient basis,” according to court documents reviewed by HousingWire.This is the second such case that has put an enforcement action on hold due to the pending constitutionality decision, according to reporting from Reuters and a blog post by ACA International, a trade association for the debt collection industry.In February, the high court agreed to hear the case involving CFSA roughly four months after a Fifth Circuit Court of Appeals panel ruled that the funding structure of the CFPB was unconstitutional. The Biden administration had hoped to fast-track the proceeding, but the court is not expected to render its decision until sometime next year.The plaintiffs in the original case, Community Financial Services Association of America and Consumer Service Alliance of Texas, challenged the CFPB’s structure, its powers granted by Congress and the director’s protections from removal, claiming all were unconstitutional. A lower court agreed, causing the CFPB to appeal the ruling to the Supreme Court, arguing in its certiorari petition that the previous decision relied on an erroneous understanding of the Appropriations Clause.The Supreme Court heard another challenge to the CFPB’s constitutionality in mid-2020, when Seila Law LLC v. Consumer Financial Protection Bureau asked the Court to determine whether the CFPB’s substantial executive authority violates the Constitutional principle of the separation of powers between the branches of the federal government.In that case, the Supreme Court ruled that the appointed director of the CFPB is not insulated from being fired by the President of the United States, but stopped short of invalidating the agency’s structure. Certain housing-related organizations including the the Mortgage Bankers Association (MBA) and the National Association of Home Builders (NAHB) previously urged the court to consider the implications of its decision.

Read MoreFinCEN crackdown on real estate money laundering expected this month

After years of discussion, the U.S. Treasury Department is expected to propose a rule that would effectively end anonymous luxury home purchases in the coming weeks, according to the Financial Crimes Enforcement Network’s (FinCEN) regulatory agenda.The rule, which department officials first said they planned to implement in 2021, would require real estate professionals, such as title insurers, to report the identities of beneficial owners buying real estate in cash to FinCEN. The department believes the proposed rule will close a loophole that allows corrupt oligarchs, terrorists and criminals to hide illegally obtained funds in U.S. real estate.According to a state from Treasury Secretary Janet Yellen in March, as much as $2.3 billion was laundered through U.S. real estate between 2015 and 2020, a trend that she said has been going on for decades.The new rule would replace FinCEN’s current reporting system known as the Geographic Targeting Orders (GTOs).The GTOs require title companies to identify the people behind shell companies used in all-cash purchases of residential real estate. As of mid-August 2023, 34 cities and counties throughout the U.S., including Litchfield and Fairfield Counties in Connecticut; Adams, Arapahoe, Clear Creek, Denver, Douglas, Eagle, Elbert, El Paso, Fremont, Jefferson, Mesa, Pitkin, Pueblo, and Summit counties in Colorado; Boston; Chicago; Dallas-Fort Worth; Las Vegas; Los Angeles; Miami; New York City; San Antonio; San Diego; San Francisco; Seattle; Washington, D.C.; Northern Virginia and Maryland (DMV) area; the city and county of Baltimore; the Hawaiian Islands of Honolulu, Maui, Hawaii and Kauai; and Houston and Laredo, Texas.In all of these GTOs, except for the city and county of Baltimore, which has a threshold of $50,000, all cash purchases of $300,000 or more must reported to FinCEN.Officials have also been working on implanting a related rule that would force real estate professionals to report the identities of shell company owners who purchase real estate in cash through their shell company. While the American Land Title Association has expressed support of the new rule, it has also stated that its implementation should be delayed until the shell company rule is also complete. The proposed rule will be open to public and industry feedback once it is announced

Read MoreBetter.com’s improbable IPO proposal is approved

New York-based digital lender Better.com will be going public via a merger with special purpose acquisition company (SPAC) Aurora Acquisition Corp. nearly two years after Better’s initial timeline to IPO. “At least 65% of the outstanding ordinary shares of the company entitled to vote at this meeting have voted in favor of (the) proposal,” Arnaud Massenet, CEO of Aurora Acquisition Corp, said in a shareholder’s meeting on Friday. The transaction, once finalized, will infuse the combined entity with $750 million in new capital, Aurora’s filing with the Securities and Exchange Commission (SEC) in July noted.Better’s SPAC deal with Aurora had been extended three times amid unfavorable market conditions, mass layoffs, huge financial losses and a mountain of bad press.Founded in 2014 by CEO Vishal Garg, Better has been making headlines for its layoffs since it gained notoriety by laying off about 900 employees over Zoom in December 2021.The lender cut about 91% of its workforce over an 18-month period, Aurora’s filings with the SEC in July showed. As of June 8, Better had about 950 team members, down from its peak of about 10,400 employees in Q4 2021.Another controversy that didn’t help Better’s IPO was an SEC investigation over allegations Garg misled investors ahead of a planned SPAC merger. The SEC recently concluded it doesn’t intend to recommend an enforcement action against Better. The digital lender posted a net loss of a net loss of $888.8 million in 2022 and $89.9 million in the first quarter of 2023, according to the SEC filing. Better funded 2,347 loans in Q1 2023, a decline of 87% compared to 18,559 loans funded in Q1 2022. Better recently pivoted its real estate strategy, laying off its in-house brokerage subsidiary and partnering with outside agents.Better ranked as the 59th largest mortgage lender in the country in the first quarter, according to Inside Mortgage Finance. Aurora’s shares were trading at $37.03 on Friday morning after the vote, down 8.77% from the previous closing. Aurora’s share price skyrocketed 530% to $62.91 after the SEC declared the SPAC combination effective.

Read MoreFreddie Mac’s updates to the ACE + PDR valuation option

Appraisal modernization is a hot topic right now, but updating the appraisal process is easier said than done. The process today is limited by a number of structural constraints, according to Scott Reuter, Single-Family chief appraiser at Freddie Mac.While the industry as a whole has been adopting new technology, the appraisal process has remained relatively unchanged — right down to the forms used to complete them.Another difficulty with appraisals historically has been appraiser capacity. Over the past decade, the number of active appraisers has remained static. In the current market, where volume has decreased, this is less of a concern. In markets with higher volume, such as 2020-2021, it can be difficult for appraisers to keep up with demand — which slows loan processing times and drives up costs for borrowers.Reuter also noted that appraiser capacity in future high-volume markets may also be strained by appraisers aging out of the profession and retiring.“Depending on which study you look at, 70-75% of appraisers are older than 55,” he said. “10 years out, the industry may be losing some appraisers to retirement in an already strained industry and there’s a lack of inflow of new appraisers.”Freddie Mac’s appraisal modernization strategyWith these challenges in mind, Freddie Mac continues to work on modernizing the appraisal process for lenders that deliver loans to Freddie Mac. “The approach is twofold,” said Kevin Skowronski, Collateral Risk Policy Senior at Freddie Mac.“First, we’re looking to modernize the traditional appraisal process and the forms that have been required into something that is more data-driven, flexible and dynamic,” he said. “The second part of the strategy is to offer a wider variety of valuation options.”“From a modernization perspective, we want to promote consistent and fair valuation outcomes, simplify the loan manufacturing process, reduce borrower costs and effectively manage risk. If we can check those boxes, we succeed. We apply this approach across a spectrum of valuation options from traditional appraisal to our automated collateral evaluation (ACE) appraisal waiver, and we’re focused on what we can do between the ends of the spectrum.”“Risk mitigation heavily informs Freddie Mac’s strategy,” Reuter added. “All of the valuation options and enhancements we’re thinking about testing have to pass that first bar of not introducing any additional risk to Freddie Mac,” he said.ACE+ PDR: An enhanced optionOne of Freddie Mac’s newer valuation options, which has been in effect since July 2022, is ACE+ PDR, or automated collateral evaluation plus property data report. With a PDR, property information is physically collected on-site by a trained property data collector, who prepares the PDR identifying property characteristics and capturing photographs. The PDR provides property data information, which can help mitigate risk.ACE+ PDR was originally a temporary offering. However, effective August 2, 2023, this offering has been added to the Single-Family Seller/Servicer Guide (Guide). While ACE+ PDR was previously available only for refinances, the eligibility has been expanded to include eligible purchase transactions. That means more opportunities for lenders — and their borrowers — to benefit from loans originated without an appraisal.“ACE+ PDR fits right in line with our approach to collateral valuation and appraisal modernization. We’re always looking for new ways to deliver value to the housing ecosystem,” Reuter said. “Whether that’s to allow appraisers to focus on the more difficult assignments, help lenders efficiently originate loans or achieve potential cost savings for borrowers.”“On lower-risk loans during busy times, lenders may not necessarily have to get a full appraisal — there are other options,” Reuter said. “We’re trying to responsibly leverage data and technology to save time and reduce costs in the origination process through different valuation options.”The PDR can be completed by a trained property data collector, as long as lenders meet the requirements outlined in Freddie Mac’s Guide.“Freddie Mac has certain property data points in its dataset,” Skowronski said. “We require property data collectors to be trained on the dataset so they can understand the data points, the allowable enumerations and the expected responses.”Property data collectors are also trained on how to identify observed issues about a property that could require repairs or an outside inspection, as well as how to measure a property and accurately produce a floor plan with measurements and calculations.“The property data collector may be a non-appraiser, appraiser or appraiser trainee, but must meet certain requirements and be appropriately trained,” Skowronski said. “Individuals already in the housing industry, such as real estate agents or home inspectors, may become property data collectors too.”Reuter and Skowronski said that Freddie Mac will continue to evaluate the PDR process to see how it evolves in the marketplace.“It won’t be applicable for every economic cycle, but there will be instances where having alternative approaches benefit the industry and reduce time and cost while ensuring the same level of risk mitigation,” Skowronski said.“Freddie Mac will continue to modernize the valuation process,” Reuter added, “leveraging emerging tools and technology while maintaining a risk-informed approach.”“Appraisals, at the end of the day, are and will remain an important part of our risk management process while we continue to monitor and modernize the valuation process,” he said.Sign up to receive collateral valuation and appraisal insights, best practices and resources from Freddie Mac.

Read MoreREIT fight: Western Asset agrees to merge with AG Mortgage after spurning Terra

AG Mortgage Investment Trust, Inc. entered into a definitive agreement Tuesday to merge with Western Asset Mortgage Capital Corp., beating its competitor Terra Property Trust, Inc. AG Mortgage, a pure-play residential mortgage REIT controlled by Angelo, Gordon & Co. and owner of mortgage lender ARC Home, made a stock-and-cash offer for its peer Western Asset, managed by Franklin Resources, Inc. As a result, Western Asset terminated its previously-announced acquisition agreement with Terra Property. The AG Mortgage deal includes the payment of $10.11 per Western Asset common share and $1.12 in cash per share, representing a transaction value of $11.23 per share, a 34% premium on Western Asset’s closing stock price on the NYSE on July 12, 2023.“Combining these highly complementary portfolios will help scale our platform, generate greater operational efficiencies, cost synergies, and accretive earnings growth, and benefit all stockholders,” T.J. Durkin, president and CEO of AG Mortgage, said in a statement. Last year, Western Asset, a non-qualified-mortgage player, announced it was exploring a potential company sale or merger after posting a $22.4 million net loss for the second quarter of 2022. The dispute between AG Mortgage and Terra Property began two months ago. On June 28, Terra Property, managed by Mavik Capital Management, and Western Asset announced that they entered into a definitive agreement to merge in a book-for-book deal. The transaction valued Western Asset at $17.30 per share, but the REIT’s stocks traded down after the deal became public. Investors were skeptical about Terra Property’s share value since it’s a non-traded REIT. On July 13, AG made its first offer for Western Asset at $9.88 per share, including $0.98 in cash. The bid included an implied value of $8.90 per common share ($54.5 million in total) and $0.98 per share in cash to shareholders ($6 million in total). AG Mortgage waived $2.4 million in management fees in the first year after closing.Terra Property then enhanced its proposal, offering an implied share price of $15.96 per share, including $1.43 per share and $8.75 million in cash, but Western Asset declined. Vik Uppal, chairman & CEO of Terra Property and Mavik Capital Management, expressed disappointment with the response to its proposal that he felt demonstrated “superior value.” ““[Western Asset] requested additional changes that we were unwilling to make because they would not have been in stockholders’ best interests, ” Uppal said in a statement. Bonnie Wongtrakool, Western Asset CEO, said the merger with AG Mortgage delivers immediate cash value to Western Asset stockholders and will let them continue to participate in the upside of the combined company.

Read MoreThree Trends Impacting New York City Commercial Real Estate

Tenant behavior in the office market, regulation in multifamily and higher interest rates contributed to a 43% drop in NYC investment sales to $12.8B in 1H 2023.

Read More-

A winery for sale in Southern Oregon checks all the boxes: thriving vineyards, riverfront location, rolling meadows, mountain views and plenty of space to expand.

Read More Freddie Mac releases 2023 stress test results

In accordance with the Dodd-Frank Wall Street Reform and Consumer Protection Act, Freddie Mac has released its 2023 Stress Test Disclosure, which reflects two hypothetical economic scenarios, including a “severely adverse” scenario. Under the latter, Freddie Mac would face a credit loss of $13.7 billion — or 0.4% of its total portfolio — under the adverse scenario.Losses under the 2023 scenario are higher when compared to the results of the 2022 test. Last year, the GSE was projected to face a credit loss of only 6.3%, or 0.19% of its average portfolio balance.Fannie Mae has not yet released the results of its 2023 Dodd-Frank Act Stress Test (DFAST). In June of this year, that GSE was forced to re-release the results of its 2022 test after it had made an “identification of errors in an underlying model.” This led the GSE to advise against “rely[ing] on the information in [the] report for any purpose.”Freddie Mac is required to conduct annual stress tests in an effort to “assess capital adequacy under [the Federal Housing Finance Agency (FHFA)’s] rule implementing the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank) stress testing requirements,” the results explained.The annual tests are designed to determine capital adequacy, and summarizes results based on a “severely adverse” scenario prescribed by FHFA based on a hypothetical scenario that illustrates the resiliency of the model to challenging economic conditions.This year’s adverse scenario requires a 38% decline in home prices, a 40% reduction in commercial real estate prices, and a severe global market shock with the GSE’s largest counterparty defaulting.The GSE is also required to disclose “certain capital information, such as net worth, and available common equity tier 1 (CET1) calculated in accordance with requirements of the FHFA Enterprise Regulatory Capital Framework (ERCF) Rule,” a requirement which began with the publication of 2022’s results.“Results are not expected outcomes,” Freddie Mac said. “They are modeled projections based on hypothetical economic conditions. Actual outcomes may be very different.”Once Freddie Mac releases its 2023 DFAST, FHFA is expected to compile a report featuring both sets of results.Earlier this month, Freddie Mac reported that it had generated $2.94 billion in net income in the second quarter, up 41% from the first quarter and 20% year-over-year.

Read MoreMortgage delinquency rate falls to lowest level since 1979

The Mortgage Bankers Association (MBA) reported that the mortgage delinquency rate fell to its lowest level since it began tracking this metric 43 years ago, supporting claims the economy is on the cusp of a turnaround.“Buoyed by a resilient job market, homeowners are continuing to make their mortgage payments,” Marina Walsh, the MBA’s vice president of industry analysis, said in a statement.The seasonally-adjusted delinquency rate for one-to-four-unit residential properties stood at 3.37% in the second quarter of this year, down 27 basis points compared to the same period one year ago and 19 basis points quarter over quarter, the MBA reported. The percentage of loans on which foreclosure actions were started in the second quarter fell by 3 basis points.Delinquencies across all mortgage types, including conventional, FHA, and VA mortgages fell during the second quarter. Despite this encouraging news, the MBA reported some signs of consumer-related stress, with delinquencies rising for other forms of credit, including credit cards and car loans, noted Walsh. In addition, FHA delinquencies rose 10 basis points compared to the year-earlier period, and on a non-seasonally adjusted basis, rose 13 basis points year over year and 71 basis points from the first quarter of 2023.“As the economy slows and [the] labor market cools, homeowners with FHA loans are likely to feel the distress first,” said Walsh.

Read More‘Monaco Of Mexico’ Luring Americans To Luxe Properties

Sunny beaches, eclectic dining, sizzling nightlife and more are among the drawing cards of Los Cabos, a destination boasting a growing number of luxury resorts.

Read More

Categories

Recent Posts